The Unrelenting Ambition of Airwallex

The $5.6 billion fintech has established itself in APAC. It will not rest until it wins the rest of the world.

Brought to you by Airwallex

Airwallex is a leading global financial platform for modern businesses, offering trusted solutions to manage everything from payments, treasury, and spend management to embedded finance.

With our proprietary infrastructure, Airwallex takes the friction out of global payments and financial operations, empowering businesses of all sizes to unlock new opportunities and grow beyond borders. Proudly founded in Melbourne, Airwallex supports over 100,000 businesses globally and is trusted by brands such as Brex, Rippling, Navan, Qantas, SHEIN, and many more.

For more information on how Airwallex can help you simplify your global payments and financial operations, get in touch with our team today.

If you only have a few minutes to spare, here’s what investors, operators, and founders should know about Airwallex.

- Hello, world. Airwallex has built a robust financial platform with global coverage. Its APIs and applications serve over 100,000 companies across Asia-Pacific, Europe, North America, Latin America, and beyond. That includes leading startups like Brex, Canva, and Rippling.

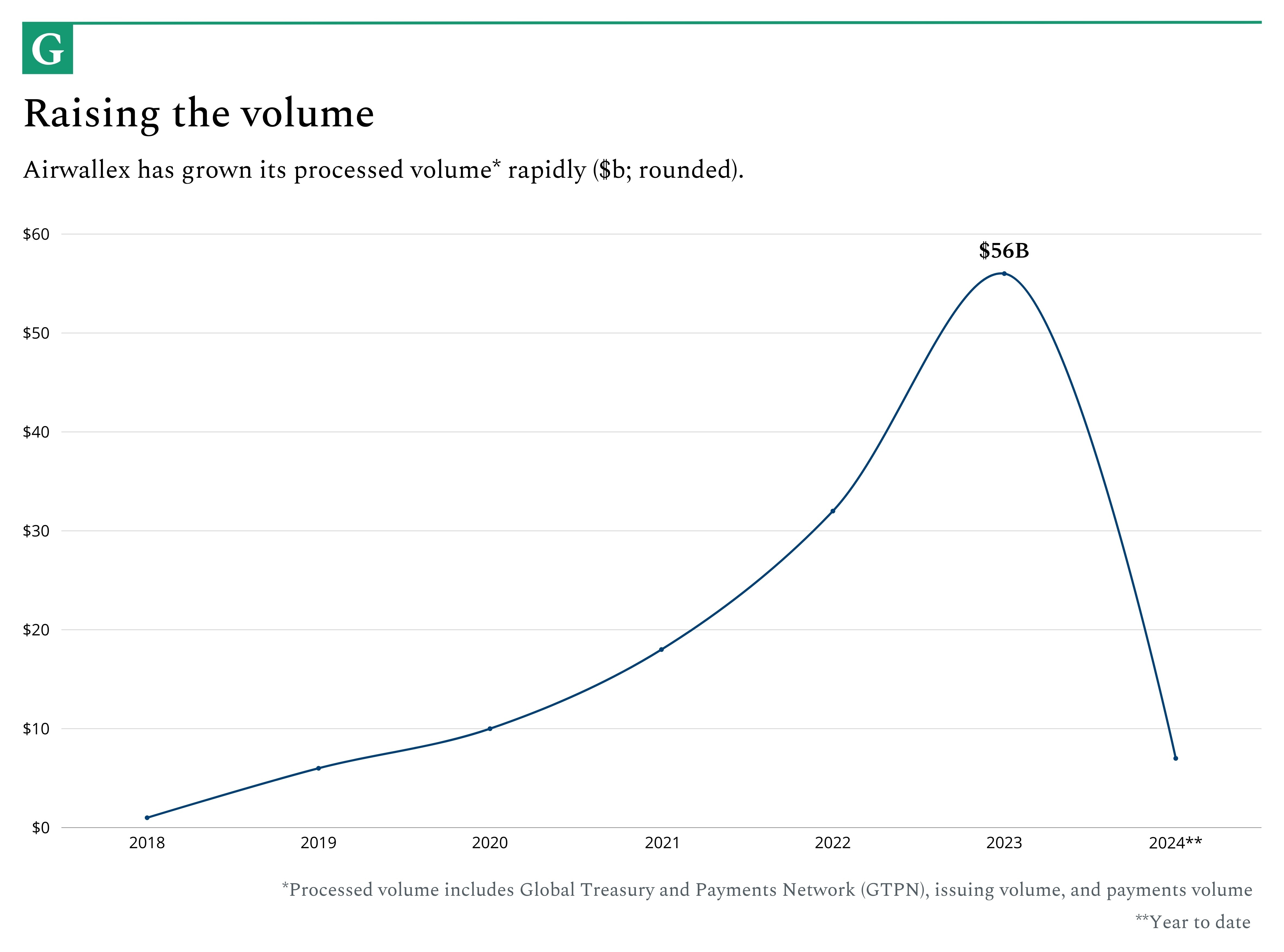

- Cash flow positive. In 2023, Airwallex reported it had turned cash flow positive for the first time. That milestone was a dividend of the company’s impressive trajectory and growing scale: Airwallex is operating at approximately $80 billion in volume run rate, with an annual revenue run rate close to $400 million. It looks increasingly well-prepared for a future IPO.

- All work and no play…Makes Jack Zhang an impressive CEO. Employees and investors refer to Airwallex’s founder as perhaps the hardest-working executive they’ve ever met. He is known for working around the clock to keep his global business spinning, with a gift for keeping the full mechanics of the business in the front of his mind, down to the most granular details.

- Culture clashes. Though Airwallex has many strengths, it has struggled to build a copacetic company culture at times. In early 2023, that issue came to a head, prompting a company-wide recalibration designed to improve communication and promote employee growth and development. Early results suggest that initiative has worked.

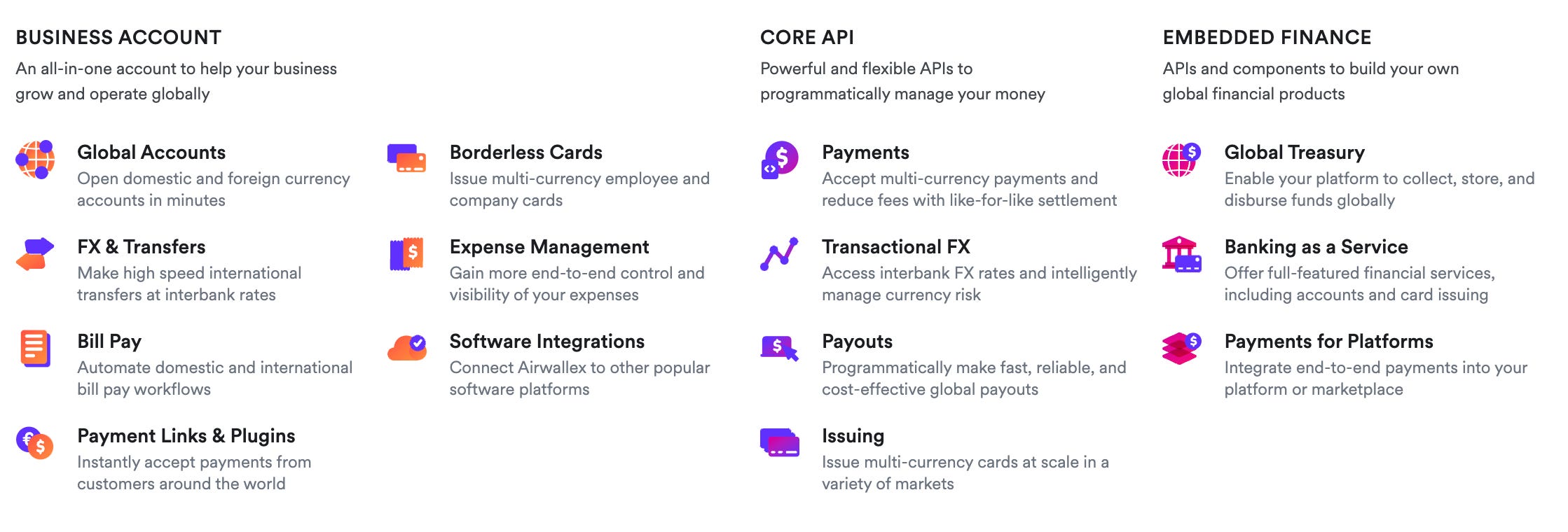

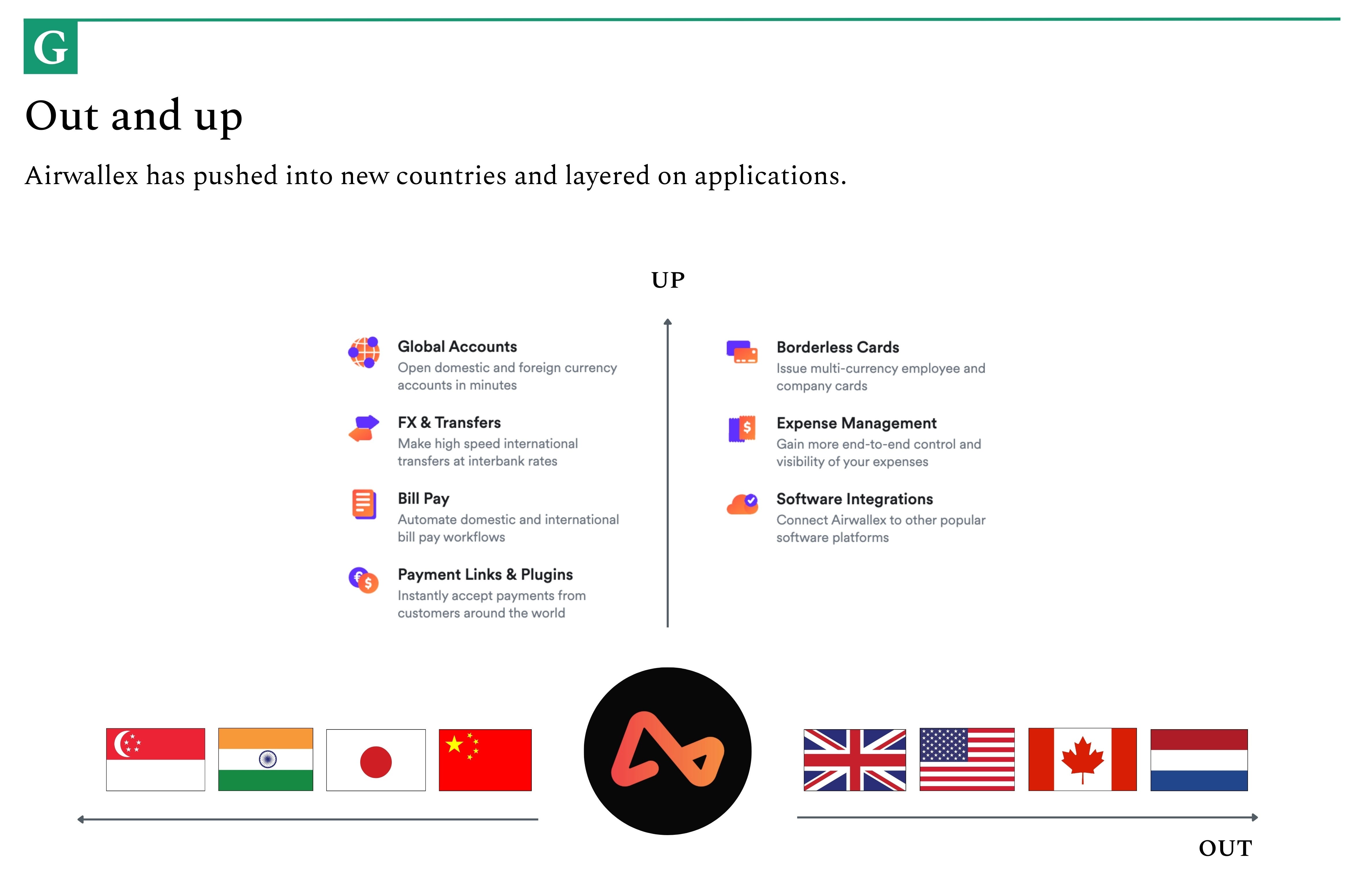

- Out and up. Airwallex has an intriguing, powerful growth expansion mechanic: it expands “out” to new geographies and builds “up” by adding new applications to its platform. Today, its product suite includes global accounts, online payments, foreign exchange and transfers, bill pay, cards and expense management, and embedded finance. Expect this growth movement to continue over the coming years.

This piece was written as part of The Generalist’s partner program. You can read about our ethical guidelines in the link above. We always note partnerships transparently, only share our genuine opinions and commit to working with organizations we consider exceptional. Airwallex is one of them.

Jack Zhang waited for his train, his body aching. To pay for his undergraduate degree at the University of Melbourne, Zhang had taken a job at a lemon factory in the mountains outside Victoria’s capital city. Each work day, Zhang woke at 5 AM to begin a more than two-hour commute, catching a train to the suburbs, switching to a bus that took him into the countryside, and walking the last mile and a bit to the processing plant for an 8:30 AM start.

For the next ten hours, Zhang repeated a simple, exhausting task: he picked up a box of lemons and loaded them into a truck. He picked up a box of lemons and loaded them into the truck. He picked up the lemons and loaded them into the truck. The weight and repetition gnawed at the muscles of his forearm, the small of his back, the soles of his feet. At half-past six, Zhang would put down the boxes – this time for the night – and reverse the long journey home.

One evening, Zhang’s train didn’t arrive. He waited for half an hour, then an hour. He realized it wouldn’t come that night only as the late Australian summer sun began to set. It was Christmas Eve.

Zhang was 30 kilometers from home, on the outskirts of Melbourne, with the sun and temperature falling. If he’d had more money, Zhang might have called a taxi service. Even on Christmas Eve, some enterprising driver would be willing to make the trip. If he’d been a different person, he might have asked a friend to pick him up.

Instead, the seventeen-year-old student turned back to the road and began to walk. Zhang can’t remember what he thought about on the long journey back to the city, but during those days, his mind tended to flow in a common direction. It streamed not so much toward an idea as an urge, a demand: More. That was what Zhang thought about as he lifted boxes of lemons into the back of a truck and what he would think about as he served drinks to businessmen at the bar of the Westin Hotel two years later. He would look at their suits and monogrammed shirts, watch as they sipped expensive cocktails, and think: I want what they have. I want more.

Zhang was willing to work to achieve his goals; in fact, he wanted to work. For as long as he could remember, he’d possessed an intensity that startled his parents and didn’t always suit the quiet conformity expected of schoolchildren in his native Shandong. The loneliness of arriving in Australia as a sixteen-year-old with little grasp of the language had sharpened that drive, as had the family financial problems that had made paying for his undergraduate education his responsibility. Though Zhang may have seemed like a timid young man to many of his classmates and colleagues, inside, he was a knuckle of potential energy, a bowstring pulled taut, a ballistic missile looking for a fitting target.

Today, Jack Zhang has more. Twenty-two years after working in the lemon factory and making the long Christmas Eve walk back to Melbourne, Zhang is the founder and CEO of Airwallex, a global fintech giant with offices in eleven countries and annual volume nearing $80 billion. Its clients include influential unicorns like Brex, Navan, Rippling, and Canva. A $100 million Series E extension, announced in October 2022, affirmed a $5.6 billion valuation. Late last year, Airwallex officially became cash flow positive. Even more impressive than these figures is the platform Airwallex has built – a multi-product suite spanning global payments, treasury, spend management, and embedded finance.

That Airwallex has reached those milestones less than eight years after Zhang co-founded it from his specialty coffee shop in Melbourne is a testament to the speed, intensity, and ambition he has cemented at its core. Though Airwallex recognized the opportunity in global payments long after rivals like Wise and Stripe, it has matured into one of the market’s power players. Established as the default choice in the Asia-Pacific (APAC) region, Airwallex has set its sights on the rest of the world, opening offices across North America, Europe, Latin America, and the Middle East with encouraging results.

It has not been a straightforward journey – less a country bus commute than a Shinkansen ride on kinked tracks. By Zhang’s count, Airwallex has nearly died three times and nearly been bought once, with a $1.15 billion offer from Stripe in 2018 rebuffed at the eleventh hour. To reach its current station, Airwallex has foiled scammers, wrangled regulators, outmaneuvered competitors, and occasionally, fought with itself. Though Airwallex would not exist without Zhang, and it is impossible to picture a rosy future devoid of his surging will to power, it is also true that missiles do not make easy managers.

Former employees have voiced concerns about Airwallex’s high-pressure culture and overreaching leadership in recent years. Review sites paint a checkered picture, and low employee satisfaction ratings recorded early in 2023 quantified the unease. Many high-growth companies experience operational and cultural challenges as they morph from scrappy startups to multi-pronged enterprises at warp speed, but if Airwallex is to fulfill its generational ambitions, it will need to durably improve on this front. Great companies cannot afford to churn through talent or expect to get the best out of a wearied workforce.

To Airwallex’s credit, it has recognized this weakness and acted to correct it. The past two years have seen the firm bolster its people function, revamp internal communications, institute new employee reviews, and more granularly measure engagement. Reports viewed by The Generalist, shared for the first time, show a culture moving decisively – if not unilaterally – in the right direction. But culture changes over years, not months, and only time will show whether the trend continues. For Airwallex to reach Zhang’s goal of eclipsing the world’s biggest financial companies, it must maintain its momentum.

In addition to studying Airwallex’s cultural transformation in action, The Generalist has spent five months reviewing internal and external collateral and interviewing leadership, investors, employees, and customers. In total, we spoke with more than fifteen sources; many of their stories and commentary are being published on the record for the first time. The result is a portrait of an impressive but complicated company, a detailed chronicle capturing Airwallex’s serendipitous founding, remarkable growth, and unrelenting ambition.

The outsider

Stare at it long enough, and you can see what people mean when they say China is shaped like a rooster. Pull the map up in front of you, activate a cloudwatcher’s gaze, and it appears. The beak sits in the northeast, peering over Vladivostok; the chest holds Shanghai, proudly puffed towards the sea, and the tail feathers sweep across disputed Tibet up to the fringe of Central Asia.

Jack Zhang was born on one of the rooster’s errant feathers in 1985. The province of Shandong sticks out from Mainland China, jutting into the Yellow Sea and toward the Korean peninsula. Though Shandong is the country’s second most populous province, Zhang was raised in a “small town” on the outskirts of one of its major coastal cities. His parents worked at large domestic banks, putting them in China’s upper middle class. Zhang’s father held a particularly illustrious position, overseeing thousands of employees as one of China Construction Bank’s regional managers.

Zhang’s parents did not take long to realize their son was unlikely to repeat the reliable, orderly path their careers had followed. From a young age, Zhang evinced an outspokenness that even he finds difficult to articulate decades later. “My parents always felt that my personality is a bit…” he began in our conversation, trailing off and thinking for a moment. “A lot of the kids – you tell them to do something, and then they will do something. I’m always very vocal about things, how things should be done. I never really listened to my parents. I was always creating a bit of trouble.”

Zhang might have been a troublemaker, but he was no truant. Though he struggled to keep his opinions to himself, he found little trouble applying his intense, hyperactive mind to his studies. In those days, Zhang was more interested in accumulating social capital than financial capital, with his intellect providing a steady flow. He was known as one of the district’s best students by his early teenage years. “I think generally people respected me as ‘academically strong,’” he recalled.

A coveted extra-curricular post as head of a student-run magazine called Urban Exploration fortified his stature. It also gave Zhang an early taste of independent work and the satisfaction of running something. “It was one of the inspirations that made me want to do things,” he said. “Like do interesting things.” Urban Exploration also gave Zhang an outlet to talk about one of his passions: computer games. Like so many other tech entrepreneurs, Zhang discovered software engineering through these games, spending free time playing titles like Counter-Strike on his desktop.

Despite his precocity, Zhang’s parents still worried about him. His headstrong demeanor might not have impeded him yet, but it was an uneasy fit with the surrounding environment. “In China, if you’re very vocal about things, that’s not necessarily a very good thing,” Zhang said. “That’s why they decided to send me to Australia.” A more liberal atmosphere would give their teenager a better chance to fulfill his potential.

Within the Western world, Australia was a practical choice. The United Kingdom was considered too expensive, and America, in the aftermath of 9/11, didn’t seem particularly hospitable to immigrants. Zhang’s father traveled to Melbourne to assess the city alongside a few other Chinese parents who were considering sending their children abroad. In late 2001, Jack arrived in the antipode alongside four other Chinese students, settling in time for the start of a new Australian school year.

It proved a startling change. “I was used to [seeing] cosmopolitan cities, and you go to Melbourne, you go to my school, and there are sheep and horses, and you can’t really see any buildings.” Even small details conspired to Zhang’s feeling of dislocation. His unfamiliarity with the language and surrounding environments often led to him getting lost in Melbourne’s suburbs. “I just have a terrible sense of direction. I got lost all the time. Because I [didn’t] recognize some of the bus stops or whatever, like, I just constantly [got] lost.”

The greater shift occurred in Zhang’s inner landscape. “I went from, academically, the top 100 in my school to some random student that didn’t speak English very well,” Zhang recalled. The social status he had enjoyed as the student leader of Urban Exploration also evaporated beneath the Victorian sun. “Going from that to [becoming] nobody [was] very interesting. [It makes] you want to do something, right? You want to get back to where you were.” Australia may have offered a freer environment better suited to Zhang’s forthrightness, but that meant little for someone who didn’t have the language to express themselves. Though in the long run, moving to Melbourne allowed Zhang to flourish, in the short term, it seemed to harden something in him, sharpen his desire to prove his abilities.

High school was a drab, lonely period in Zhang’s life. “It was very difficult to make friends,” he said. “There [were] literally less than ten Chinese folks in my school, and most of them were from Hong Kong and Macau. At that time, there was a bit of racism from [them towards] anyone from the mainland.” Even amongst his compatriots, Zhang felt like an interloper. “You always feel you’re kind of the minority in society.”

The challenge of learning in a new language muted the impact of Zhang’s natural intelligence. He graduated high school in 2003 with improved English and a place at the neighboring University of Melbourne to study computer science.

It was at university that Zhang met Jacob Dai. In many respects, the young men had lived parallel, though subtly different lives. Like Zhang, Dai had been an exceptional student in his native China before emigrating to Australia in high school. Unlike Zhang, a boisterous personality hadn’t been the cause of Dai’s departure – his Chinese high school held a partnership with an Australian institution, and Dai was simply excited to experience life in a new country.

An encounter at one of the university labs evolved into an easy friendship marked by a shared interest in technology. The pair would frequently work on school assignments together and discuss the merits of alternate approaches. “I was always working with Jack…[discussing] a different solution to solve the same problem,” Dai said. That ability – to tackle a challenge together, but from disparate angles – would prove invaluable in time.

Other lives

Zhang had more pressing problems in the short term, however. A change to his father’s job at China Construction Bank radically impacted his earning potential. To support her son’s schooling, which was especially expensive at that time because of the disadvantageous exchange rate between Aussie dollars and yuan, Zhang’s mother left her job and started a company of her own, selling internet voice calling solutions to local Chinese businesses. It was a tough job that required constant hustle and offered little security. “The only reason she [did] that was to support my [studies],” Zhang said.

Zhang had worked in high school, scrubbing dishes at a local restaurant, before eventually graduating to some light cooking duties. His family’s financial difficulties meant employment was no longer optional but mandatory. To try and maximize his earning potential, Zhang sought out arduous, manual work – a job that would pay an above-market rate because it had to.

And so Jack Zhang arrived at the lemon factory and began to lift boxes. There is something telling in that when he recounts that job today, Zhang is casual about the length of his circuitous commute and the fatiguing nature of the work. What seems to annoy him most is not the effort he expended but that one of his co-workers didn’t share his industriousness. “The other guy [tasked with loading boxes] was the boss’s son,” Zhang said, eyes glinting with ferocious humor. “And he doesn’t do shit.” Much of Zhang’s next two decades would center around finding a home for his intensity – and colleagues who shared it.

Not all of Zhang’s odd jobs required quite as much perspiration. Standing behind the bar at the Westin Hotel, fixing drinks for Melbourne’s businessmen, ignited his envy but didn’t require the same backbreaking exertion. Watching a mid-level ad executive in a chambray suit sip a martini, Zhang felt it might take relatively little to make him happy. “I look at all these people drinking in a bar. I was like, ‘Ok, I would prefer to be drinking in a bar and having a decent job and wearing a suit to work every day.’” The world he wanted tantalized within touching distance but remained out of reach.

Zhang had the energy, the ambition, the drive, but lacked the knowledge of how to apply it. He also did not know just how far it could take him. As he approached his college graduation, that gulf continued to show itself. Classmates applied to job openings he never saw at companies he didn’t know existed. “They would say, ‘Oh, I would love to go to Goldman Sachs,’” he recalled. “And I would ask stupid questions like, ‘What is Goldman Sachs?’” Everyone around him seemed to be better prepared and better networked – to have a better plan for their lives.

Zhang’s frenzied employment schedule had taken a toll on his studies, leaving him with a middling academic record. Combined with the absence of permanent residency status, that complicated his post-university job search. “I applied to all the investment banks and [almost] all of the consulting companies. They all rejected me, never got an interview.”

In the end, Zhang secured an engineering position at insurance multinational Aviva, one of just two graduates. That he was successful in his application owed much to his tendency to answer even boilerplate questions with unvarnished bluntness. When he asked his manager later why he’d hired him over hundreds of more outwardly impressive candidates, Zhang was reminded of one of his responses. “He asked me, ‘What is your plan for the next three to five years?’ And a lot of the people [he interviewed] were well prepared. It’s like, ‘I want to be a senior engineer, or I want to be a manager in five years.’ Whatever. When I look at that question, I’m like, ‘I have no idea what I’m going to be doing in three to five years. But one thing I know is that I’m going to try to figure this out very, very quickly by working really, really hard.’ That was quite an honest answer. He’s an engineer, he likes honest answers. That’s how I got the job.”

Zhang did work very hard – both in and out of the office. At the same time as he worked for Aviva, he broke ground on several side projects. The first was a derivatives trading algorithm that quickly racked up major wins. “It looked at different historical data and tried to trade a certain trend,” Zhang explained. It worked frighteningly well. In less than a year, Zhang’s system – which he had coded himself – turned a few thousand dollars into $500,000. The student who had sorted citrus to pay for his schooling had become a demi-millionaire before his Goldman Sachs-chasing classmates could secure their first bonus.

It took Zhang even less time to lose his earnings. The onset of the Global Financial Crisis in 2008 rocked markets and scuppered the software developer’s algorithm. In just three days, Zhang lost everything. “It only worked in certain market conditions,” he chuckled.

Rather than cow him, the disintegration of Zhang’s bank balance seemed to embolden him. He rebuilt his trading algorithm to operate more conservatively. He started an export business, selling Australian red wine and olive oil to overseas purchasers. And, alongside fellow University of Melbourne alum Max Li, he began to tip his toe into real estate.

Though Zhang had no experience in the sector, he had natural commercial instincts and an innate work ethic. Combined with Li’s architectural expertise – he had gotten his Masters in the discipline – they made a compelling team. Together, they founded a real estate business: Li handled the design, and Zhang took care of the operations. Zhang kept the venture growing before and after work, on the weekends, and during whatever breaks he could steal from Aviva and his next employer, National Australia Bank. Soon enough, he and Li graduated from handling simple residential properties to larger commercial ones. Bit by bit, Zhang’s bank account crept closer to its previous high – then surpassed it.

Diverging

By 2013, he and Li were ready to push their business to the next level. It was in observing a difference between their native China and new Australian home that the pair spotted an opportunity in the food and drink industry.

More than London, Milan, or New York City, Melbourne is increasingly regarded as the epicenter of coffee culture. Home to more than 2,000 cafes, the Australian city has spawned the “flat white” phenomenon, followed by a trail of “magics” and “piccolos” heading to your trendy neighborhood coffee shop in the coming years. Such ubiquity was already well established by 2013, starkly contrasting Zhang’s native China. When he returned home, he noticed the scarcity of specialty shops.

The absence of a coffee culture in China was the product of a commercial reality, but one that Zhang and Li felt was primed to change. Older generations hadn’t much of a taste for lattes and cappuccinos, but their more cosmopolitan children increasingly did. “We see that my generation and below, those that were educated in the West – they start [having] a lot of demand, a lot of consumption ability,” Zhang said. “So we see a trend of specialty coffee getting very popular in the region. [That’s what] we thought! But at the time, it hadn’t happened.”

It was a shrewd reading of the market. In the eleven years since, a rush of established and insurgent coffee brands, such as Peet’s, Tim Hortons, SeeSaw, Manner, and Luckin, have flooded the Chinese market.

Zhang and Li devised a plan. They would start by opening a coffee shop in Melbourne to test their concept and work out the kinks. After all, that was where both of them lived and had built their real estate expertise. They would not treat it like their other projects, though. Rather than building it bespoke, they would orient every detail to be replicable, extensible across dozens, perhaps hundreds of stores. “I [was] thinking about building something like a Blue Bottle. We build everything so you can franchise, so you can build many shops. Everything we designed is designed [for the] mass market. It’s not designed just to build one shop.” Once they succeeded in Australia, they’d move to China and begin in earnest.

Before it opened its doors, Zhang and Li’s coffee concept nearly repaid their efforts many times over. In thinking about maximizing their store’s throughput, Zhang began exploring point-of-sale (POS) solutions. Although Square existed in the United States, it had yet to reach the Australian market. Though Zhang looked, he couldn’t find a good domestic solution that allowed customers to use near-field communication (NFC) technology to make purchases with their phones. Why not build one?

A conversation with his college friend Jacob Dai dissuaded Zhang. After staying on for a Master’s in software engineering, Dai had embraced innovation’s unpredictable frontier. His first job after graduation had been at an online payments startup. Like Zhang, the Global Financial Crisis had altered his trajectory; in its wake, Dai’s employer failed to raise capital and shuttered its doors. A slew of other tech jobs followed. In China, Dai worked at an artificial intelligence startup that used its technology to help internet companies censor pornographic images, followed by a spell at a “smart loudspeaker” upstart. Zhang was impressed by Dai’s eclectic experiences, deep technical expertise, and knowledge of alchemic technologies like artificial intelligence.

Dai didn’t like the point-of-sale pitch. It was too small, too short-term, he told Zhang. “[Jacob] was like, ‘This is a shitty idea. NFC is going to become the past. In China, it’s all QR code – QR codes are going to take over the world,’” Zhang remembered. “I’m like, ‘Ok, maybe this is not a good idea. So we gave it up.” With a rueful laugh, Zhang reflected on the commercial implications of this unpursued path. “I think our business is probably even bigger today if we got there earlier. Because this is like two or three years earlier than Airwallex [was] founded.”

In 2014, Zhang and Li opened Tukk & Co. in Melbourne’s Docklands neighborhood. It offered good coffee (and burgers) in a popular location – just a stone’s throw from the city’s Marvel Stadium. Alongside a steady supply of regulars, Tukk could count on the intermittent traffic of Australian Football League fans and concertgoers.

Tukk & Co. matured into a viable and profitable business. But the shop’s habit of introducing its founder to interesting problem spaces proved even more useful than its steady cash flow.

Like many businesses, big and small, Tukk relied on imports. Packaging, straws, napkins, and other materials were bought from overseas suppliers and sent to Australia. While that process helped keep Tukk’s costs in check, it introduced considerable financial and operational overhead. For a vendor in China to receive payment, Tukk needed to find a way to convert its Australian dollars into yuan and then have the converted sum hit the seller’s correct bank account. Making that happen involved back and forths with banks in both countries, a hefty foreign exchange (FX) fee, and significant delays. In 2015, Zhang found himself wondering why there wasn’t a better solution – and if he should build one.

Other factors impacted Zhang’s growing interest in a new chapter. His investments and real estate exploits had made him wealthy, giving him a life that his younger self would have intensely envied. He was thirty, married, and a multi-millionaire. He had a young daughter approaching her first birthday. Yet he couldn’t help feeling a sense of dissatisfaction, a kind of festering discontent.

Sure, he liked his job as a software engineer at ANZ, one of Australia’s “Big 4” banks. It kept him busy and gave him a place to practice his craft. “I had a full-time job because I love writing code,” he said. But it felt vaguely pointless. What did he want out of it? A pay raise? A promotion? He already earned ten times his managing director’s salary outside the office. Zhang wanted to keep writing code, but do it somewhere that could match his velocity. When he held his daughter, he couldn’t help but feel unimpressed by his achievements. “I look at her, I was like, ‘I haven’t done anything that [makes] her proud,’” Zhang said. “I want to do something different. I want to do something meaningful to the world that she feels she is proud [of] her Dad.’ That’s why I resigned.”

Zhang’s last decade had taken him far. He hoped his next would make it seem like little more than a footnote.

1,100x

In 2015, Lucy Liu went on holiday to Australia. The University of Melbourne graduate had spent the previous four years between Hong Kong and Shanghai, working for financial firms. Though stints at Barclays and CICC, a Chinese investment bank, had been advantageous for her career, she missed the friends she had made en route to receiving a Masters in Finance, as well as the Australian lifestyle.

Max Li was among the friends Liu was excited to reconnect with. A coffee aficionado, Liu looked forward to seeing his store and trying its concoctions for herself. While visiting Tukk & Co. one Friday evening, Liu and her husband were introduced to the store’s other owner, Jack Zhang. “I finished work a little early that day,” Zhang said, “I went to the coffee shop, was chatting to Max. Lucy was there. We got introduced, and we said, ‘Let’s grab dinner.’”

It was over dinner that Zhang shared his plans for the future. He, Max Li, Jacob Dai, and Ki-lok Wong – a co-worker from NAB – were going to build an international payments business to solve the foreign exchange problems they’d encountered running Tukk & Co.

It was a strong quartet, Zhang felt. Jacob Dai was a talented technologist who had already fulfilled the role of CTO at previous startups. Max was a gifted and remarkably flexible designer, capable of designing both buildings and software applications. Ki-lok Wong was the junior partner, an “employee number one” with a co-founder title and a 5% stake. As he told Liu, Zhang planned to head to Hong Kong in the new year to raise seed funding.

Lucy Liu was intrigued by the pitch and Zhang’s plan of attack. How much money did he want to raise? “I said, ‘I want to raise $1 million, and that should be enough to get us going,” Zhang recalled. He hoped to give away no more than 20% of his business in exchange for that capital, an implied post-money valuation of $5 million.

Liu surprised him. “She basically said…‘Why don’t I give you $2 million? And then you don’t need to raise any more? I’ll give you $2 million for 40% of the company.” All of a sudden, Zhang found himself in a negotiation with a counterparty he barely knew. “This is like the first time I ever met her. I don’t know what she does at all. Then she just went quite serious about it.” Liu ended the meal by suggesting the four of them meet at the University of Melbourne’s law library the next morning to discuss the details – 9 AM sharp. If Zhang had doubts about Liu’s seriousness, that suggestion disabused him of them.

Melbourne’s law library is a dull, porridge-colored building interrupted by a stripe of glass. When Zhang met Liu and her husband there the following day, he sensed a simmering tension. “Lucy’s husband was strongly against it. He was like, ‘We were going to use the money to buy an investment property, and now you’re going to invest the money,” Zhang remembered. That briefly slowed talks, but it was resolved soon enough. By noon, the parties had reached a deal: Lucy Liu would invest $1 million for 20% of the company.

Liu was capitalizing a company that technically didn’t exist. Though he’d decided to leave, Zhang had yet to give his notice to ANZ and had done none of the work to incorporate the unnamed company. On Monday morning, Zhang woke to discover that Liu’s $1,000,000 had hit his personal bank account. It felt surreal – and more than a little nerve-wracking. Over the course of a weekend, Zhang’s startup had gone from a possibility to a reality. Suddenly, he had a promising idea and actual shareholders – or he would, once he set up a cap table.

Liu’s money accelerated Zhang’s timeline and caused him to reconsider the founding team he’d assembled. “I [felt] a little obligated to look after [their money],” Zhang said. “I was like, ‘Why don’t you join us as a co-founder so you can watch us spend the money? This is a startup, there’s more than a 90% probability it’s going to fail. So then, at least you know we tried 150%. We won’t try less than that, and we will work our asses off, and you’ll know how your money is spent.” It was an unorthodox decision but one that proved effective. Liu joined as a formal co-founder, taking over finance and operations.

Few venture investments have delivered as monumental a return as Liu’s pre-seed bet on Airwallex. Today, Zhang’s firm is valued at $5.6 billion. While Liu’s stake has undoubtedly been diluted by the $902 million in capital raised, on a gross multiple basis, her initial $1 million has been returned 1,100x – with likely more to come. And yet, there was a very real moment when it looked like Liu’s money might evaporate before Airwallex shipped a usable product.

Despite pulling in his initial $1 million target, Zhang decided to head to Hong Kong all the same. While Liu’s capital had bought him some time, he knew he would need further firepower to build the product he had in mind.

Zhang received a warm reception from many of the region’s active investors. Matrix Partners’ China affiliate showed particular interest in his idea, extending a term sheet. Zhang signed, impressed by his conversations and the firm’s domestic influence. He subsequently ended discussions with nearly all other interested parties. It was a mistake.

According to Zhang, not long after he’d signed the term sheet, Matrix asked to introduce him to the firm’s managing partner. Zhang didn’t think much of it, but afterward, the firm called and said they wanted to renegotiate the deal. To the new CEO, it was a clear sign they’d lost their conviction. “They bailed…They said, ‘Oh, it should be a lower valuation.’ I can hear from [that] line that they didn’t want to invest anymore.”

It put Zhang in a tricky situation with limited leverage. Would he have to return to the investors he’d just rejected and tell them the opportunity was open again? What kind of message would that send?

Luckily, there was one firm Zhang hadn’t officially ceased discussions with: Gobi Partners. The Hong Kong firm moved to fill the vacuum left by Matrix’s retreat, offering to lead a $2 million seed round on a $10 million post-money valuation. There was a catch, though: Gobi would only wire the money after Zhang built a working MVP. It very nearly killed the business.

Peerless

Today, if an Airwallex user in Australia wants to pay a supplier in China, Hong Kong, America, or Europe, it can be managed in just a few clicks. Airwallex offers payouts to more than 150 countries across over 46 currencies. It costs markedly less than using traditional financial institutions, which often add hidden fees, and is many times easier and more flexible. If you want to send out 1,000 payments at once, or have them follow certain workflows, you can. It’s extensible and powerful but also impressively simple: an intuitive orchestration layer that sits on top of a messy web of financial institutions and connections.

Jack Zhang’s initial attempt to solve international payments looked very different. Rather than handling foreign exchange via banks and other intermediaries, Airwallex’s founding team sought to create a peer-to-peer (P2P) solution. If a business owner in Melbourne needed to pay a supplier in Hong Kong in USD – a commonly used currency in the city – all they would need to do is deposit AUD on the Airwallex platform and wait for the platform to match them with a suitable counterparty; perhaps, a Hong Kong business looking to pay an Australian company. Instead of leveraging an interbank system, the money from each party could be used to pay the other vendor; no currency needed to leave the country. By cutting out middlemen, Airwallex could offer an efficient service at a much lower cost.

It was an elegant concept, but not without its complications. For one thing, for Airwallex to match demand across currencies, it would need to assemble a large network of users. For it to work at all, there would need to be sufficient demand on both sides of the major currency pairs. You needed enough people who wanted AUD and USD to be able to make that matching work. “There was always this tricky point of like, ‘How are we going to get enough participants?’” Zhang said. This would only get trickier as the business scaled. If you wanted to add more currencies, you needed to build volume for them, too. For example, if a user wished to trade Nigerian naira for Mexican pesos, Airwallex would have to have demand for both on the platform.

Gobi Partners imposed a condition on their investment. Before their share of the $2 million round hit Airwallex’s account, they would need to see a product in action.

Back in Melbourne, Zhang and his team set to work building an algorithm to power their P2P exchange. Zhang hoped it would take no more than a month or two to create, meaning they could cash Gobi’s check by the end of the first quarter. Even if it stretched a little past that point, it would be alright; even with their new hires, Liu’s money should get them to the summer. Surely, it wouldn’t take them that long to deliver a simple proof of concept?

However, the more Zhang and Dai worked on the algorithm, the less confidence they had it would solve the inherent difficulties of their approach. How many people would they need to serve the AUD-USD pair? How much daily volume would it take to offer a reliable platform?

The months ticked by. Zhang tried to answer those questions decisively. “We kind of did a simulation, and [from that] we knew that algorithm was not going to work,” he said. “The number of participants [needed] is just too big. Even though we raised the money based on that [idea].”

The good news was that this simulation was sufficient for Gobi to formalize its investment. The bad news was that Zhang and Dai knew there was no future in their P2P architecture. If Airwallex were to succeed, it would need to start from scratch. “We did all that work and basically threw it to the bin,” Zhang said.

A lesser founder might have closed shop after the failure of the simulation, rejecting Gobi’s money in the process. There would have been little shame in it. As he had told Liu, most startups fail. He’d had an idea of how to improve foreign exchange, and it hadn’t worked. So it goes. By closing down early, he might have saved some of Liu’s money and avoided wasting Gobi’s time and capital.

Zhang wasn’t ready to give in, though. He and the team set about building an invoicing product that facilitated payments between CNY-AUD and visa-versa. Airwallex integrated with PayEco, a Chinese financial provider, to get that prototype up and running. Though smaller in scope, it solved some of the same problems, allowing businesses in Sydney to pay suppliers in Shanghai, for example.

A promising alpha set Airwallex on a better path. To fortify his company’s overseas operations, Zhang moved to Hong Kong and began building an on-the-ground team. From his new city and with the threat of immediate insolvency lifted, Zhang began to raise his sights once more. Though the invoicing product had potential, it was ultimately a point solution. Sure, it was useful to customers, but if Airwallex were going to become a truly massive business, it would need to innovate on a much deeper level. It would need to find another way to build true foreign-exchange infrastructure.

To do so, Zhang came up with an alternative. Rather than rely on a P2P model, this time, Airwallex would try to build on top of the established interbank system. In some ways, it was an even more audacious idea than his original one. Part of the reason he’d pursued his P2P approach in the first place was because no sane bank was likely to collaborate with a tiny upstart with $0 in FX volume.

Zhang reached out to his contacts in the Australian and Hong Kong financial worlds to test that assumption – and was swiftly, brutally vindicated. “I talked to my friends at some large investment banks…Everyone came back to me saying, ‘Hey, come back to talk to me when you have a few billion dollars of volume,” Zhang remembered. Such figures seemed impossibly out of reach.

In a fit of desperation, Zhang decided on a blunter approach. If his own network couldn’t help him, he’d start pitching banks cold, picking up the phone and convincing someone on the other side to give Airwallex access to the interbank markets. Zhang often strikes a straightforward tone in conversation, but it says something about his salesmanship that this directness worked. “I was quite lucky in that I just basically cold-called Macquarie Bank,” Zhang said. “A sales guy at the FX desk picked up the phone call. I just pitched the idea – ‘We’re venture backed, we’re going to be a massive business.’ And he [was] onboard! He helped us get onboarded and connected to the interbank market.”

Take a moment to digest Airwallex’s first few months of life, and you might find some obvious lessons. The rigamarole with Matrix Partners illustrates the danger of putting all your eggs in one basket; Gobi Partners’ terms and conditions demonstrate the risks of a contingent investment; and the narrowness with which Airwallex avoided rapid bankruptcy reveals the importance of running a business with some amount of financial buffer.

Jack Zhang seemed to learn none of these lessons. He continued to operate at an “all gas, no brakes” pace, trusting his ability to raise another round before Airwallex ran out of money. By the end of 2016, he found himself in nearly identical circumstances and under even greater pressure.

It all began with good news. In September of that year, Airwallex was accepted into Mastercard’s “Start Path” accelerator, a global program for early-stage fintechs. It was a promising step. As the Macquarie Bank partnership had demonstrated, Airwallex’s success was contingent on developing good relationships with incumbent banks and financial institutions. Mastercard’s imprimatur, as did its willingness to explore partnerships, held real value.

Not long into the accelerator, Mastercard’s support turned into a firm desire to invest. Because the payment processor’s venture arm did not lead venture rounds, Zhang was prompted to find a new lead investor.

That same month, Zhang pitched Sequoia China (now HongShan), run by legendary venture capitalist Neil Shen. Zhang’s pitch had changed since the seed round. The experience at Start Path had opened eyes to the size of Airwallex’s opportunity and prompted him to think beyond pure foreign exchange. “[It] opened up a lot of our vision of where our company is going,” Zhang said. “We started thinking about building a global money movement network on top of an FX trading engine – and building the primitives infrastructure to power transaction banking.”

Airwallex’s present was a long way from that gleaming future. It had no revenue, offering a simple international bill-pay solution targeted toward small and midsize enterprises (SMEs). So far, few had hopped aboard. “We couldn’t really get many SMEs at the time, and we just wanted to raise more money and figure something out,” Zhang said with typical forthrightness. “There was no product-market fit.” Jacob Dai echoed that assessment. “We didn’t really have a business. We didn’t have many customers. We just had a good mindset and a vision.”

The scale of the opportunity nevertheless intrigued Sequoia China. Shen and fellow partner Steven Ji, who lived in Melbourne, told Zhang they would invest in Airwallex’s Series A – but only if Tencent joined them. “Sequoia is like, ‘We’re not going to invest unless Tencent invests,’” Zhang recalled. Yet again, the young CEO found himself part of a provisional round. Once more, he devoted his full energies to it, alternatives be damned.

No company holds quite as august a position in China’s tech firmament as Tencent. Not only is it the country’s largest company by market capitalization, it has also seeded many of the nation’s other giants, backing Meituan, JD.com, Baidu, and Didi. The conglomerate, founded by Pony Ma, has also backed a string of global players, including Flipkart, Spotify, Nubank, and Sea Group.

Zhang’s conversations with Tencent started brightly. His pitch resonated, the firm’s due diligence checked out, and before long, a forthcoming investment was being openly discussed. “Tencent said they’re going to give us a term sheet soon, and all the investment committee members said good things,” Zhang said. “Then the term sheet was rejected by the founder.”

Zhang’s not sure what Pony Ma didn’t like about his business plan, but the Tencent CEO’s rejection left him scrambling once more. Thanks to Gobi’s capital, Airwallex’s runway had extended through to March 2017, but that was now just five months away. Through October and November, Zhang tried to revive the deal without luck.

The stress took a toll on Zhang, even if he tried not to show it. CTO Jacob Dai recalled an episode that spoke to the mounting tension impacting the young founder. “One day he came into the office. And he [said], ‘Oh, I don’t have feeling in half of my body,’” Dai said. “So Max tried to like [slap] his face and he didn’t feel anything. They went to the hospital. [When] he came back from hospital the doctor said Jack [was under] too much pressure.”

As Airwallex headed towards the end of the year, Tencent offered a lifeline. “I’m lucky the investment team at Tencent are really helpful,” Zhang said. “They were like, ‘Ok, if there’s one person that can convince Pony [Ma], it’s going to be James Mitchell, the Chief Strategy Officer.”

Zhang might have thought winning Mitchell’s approval would be the hardest. However, the real difficulty was getting into the same room as the ex-Goldman Sachs managing director. It was, after all, the holidays, and Mitchell had left for his Christmas vacation in Melbourne. “I tried every day. I couldn’t find time to meet him,” Zhang said. “I mean, who’s on holiday and wants to meet like a Series A startup?” Christmas passed, and then it was the new year. Though many of Airwallex’s team members might not have known, the company was just two months from disintegration.

On January 5, 2017, Zhang finally got his chance. The stakes had never been higher. “I remember the day super clear,” he said. “If I fail the meeting, if I can’t convince James and James can’t convince Pony, then it’s going to be done. The company is going to disappear. We said, ‘This is the most important meeting of our life. Let’s see how it goes.’”

At a Tencent office in Hong Kong, Zhang launched into his pitch. He spoke about the problems with cross-border payments, the small businesses that would benefit from the solution, and the engineering they’d already completed to build the foundation for a strong product. To Zhang’s delight, Mitchell was an eager and prepared listener, thanks to his financial experience. “He’s one of the smartest guys you will ever meet in life. He remembered that a significant portion of PayPal’s revenue came from cross-border payments. So cross-border stuff is very interesting to him. He really liked it.”

It was all going smoothly until Mitchell asked to see a demo. When Zhang tried to get Airwallex’s product to work, he encountered an error message. He tried again. The same error message popped up.

Ultimately, it didn’t matter: Mitchell was impressed despite Airwallex’s technical difficulties. A year after Zhang convinced Gobi Partners to lead a seed round, Tencent committed to a $13 million Series A, with participation from Sequoia China and Mastercard. Once again, Zhang had driven Airwallex close to the edge and emerged stronger.

Hard takeoff

“Product-market fit” is a bureaucratic term for a vague concept. It is easy enough to define (you know that thing you call your ‘product?’ Has it found a fit with a ‘market?’) but hard to grasp. What does product-market fit really look like? Where are the thresholds? How big is big? How fast is fast? When do we declare a ‘fit’ has been officially found?

Airwallex’s 2018 exemplifies what unmissable, unmistakable product-market fit looks like. At the start of that year, Airwallex handled approximately $5 million in volume; by the end, it was moving billions – and fending off an acquisition.

The year started with Jack Zhang in a familiar position: under pressure. If you think that after securing Tencent and Sequoia’s Series A Zhang modestly, moderately managed his business, you have still not quite got the measure of him. With Airwallex’s coffers replenished and customers to win, Zhang accelerated.

By the middle of 2017, Airwallex had repositioned itself to chase after larger companies. Although Zhang thought his product would prove valuable to SMEs, they were difficult to acquire, especially relative to the meager volumes they delivered. Zhang began aiming for bigger fish, starting with his investors. “We were trying to get Tencent as a customer to power the WeChat payment network outside of China,” he said.

Zhang’s conversations with HiGuide, a Sequoia China-backed travel business, summarized many he endured during this period. “HiGuide was like a Viator in Asia. They have a lot of tourist guides around the world and drivers and staff,” he recalled. “At that time, we [were] only able to pay to like a dozen countries and [they] said, ‘Come back when you’re able to have a network paying out to 40, 50 markets. So basically we just kept building the network and building the network.”

Although it would take more time for Airwallex to convince Tencent and its affiliates to hop aboard, Zhang persuaded one of his startup’s big-name investors to sign a deal: Mastercard. If Airwallex could build the features necessary to serve an enterprise of its size, Mastercard promised to send a portion of its payments to the young upstart, delivering an estimated $1 billion in volume. If Zhang could land that kind of traction, capital would come easily. For much of 2017, Airwallex’s engineers diligently chewed through Mastercard’s exacting requirements, and by fall, Airwallex’s product was up to snuff.

Mastercard opened the floodgates, and in poured…a trickle. “No volume!” Zhang remembered with exasperation. “The billion dollars promised [became], I don’t know, a million dollars?” Any hopes of a painless Series B evaporated, with money running out once more.

To keep the lights on, Zhang raised a Series A extension round at the end of 2017. Square Peg Capital’s Paul Bassat invested $6 million at a $150 million valuation cap. That Zhang secured fresh financing on favorable terms was further evidence of his salesmanship and Airwallex’s remarkably high ceiling. Since pitching James Mitchell almost a year earlier, the story had become crisper, more ambitious: Airwallex wasn’t simply going to build an international payments behemoth; it was building the next generation’s SWIFT. Although founded in 1973, that cooperative network still processed approximately 31 million daily transactions.

Though Bassat’s injection bought Zhang more time, it did little to ease the pressure as 2018 began. “This was like two-and-a-half years after starting the company, raised close to $20 million without revenue,” he recalled. “Square Peg was the last shot. If we can’t get product-market fit, if we can’t get revenue up, we’d be screwed.”

Zhang directed his attention back to winning customers. “That was the inflection point,” he said. “I got a few very large customers. A company in tuition-fee payment, a company in travel – all in APAC.”

It is worth taking a moment to reflect on the strategic value of Airwallex’s beachhead market. It was a matter of circumstance that caused Jack Zhang to focus his energies on APAC in general and Hong Kong in particular; he was a Shandong native who had founded a coffee shop in Australia. If Zhang had been born in Paris and opened a cafe in Monterrey instead of Melbourne, he might have reached a different decision. And yet a covey of McKinsey consultants could not have made a savvier choice.

For one thing, Airwallex faced comparatively little direct competition in APAC. At the time of its founding, other lucrative regions had already spawned strong players. The US had Stripe and, before it, PayPal. Europe had Wise and Adyen. Asia had produced Ant Financial, but it was still young and far from the behemoth it looked like it would become at one point. Because of each region’s cultural, technological, and regulatory quirks, moving from one to another was far from simple. China’s extreme protectionism made it especially difficult to imagine a foreign company capturing its market.

Even more importantly, China is “the factory of the world,” as Jacob Dai put it. Businesses in every country need to interface with its multitude of foundries, factories, and warehouses, yet doing so was difficult at the time. Sure, Airwallex operated in a less competitive geography, but that geography happened to be one of the largest, most connected, and most structurally important on earth. “The China outbound economy was a juggernaut that wasn’t going to stop,” one Airwallex investor remarked. “You needed a payments company to facilitate the flow of funds.” That was what Zhang had built.

This context helps explain what happened next. Airwallex’s volume took off, climbing from single-digit millions into the billions. Month after month after month, it doubled. Revenue remained minimal, but there was no doubt Airwallex had found product-market fit.

Soon, the investors were coming to Zhang. “All the investors saw the trend in mid-2018, and they basically wanted to write another check for $80 million.” This time, Sequoia China and Tencent co-led the round, revaluing Airwallex at $450 million. For Bassat and Square Peg, that represented a healthy markup: 3x in a matter of months.

Raising money would never be a problem for Airwallex again.

Stripe

Venture capitalists were not the only ones who noticed Airwallex’s success. In September 2018, Zhang received a message from the Sequoia team. Would he like to connect with Will Gaybrick? The Stripe CFO had something he wanted to discuss.

Over a phone call, Gaybrick laid out what he had in mind: Stripe was interested in buying Airwallex. An email introduction to Patrick Collison followed, leading to a meeting between the two founders in Shanghai. Conversations continued over WhatsApp in the following weeks.

According to sources involved in the deal and close to the talks, Airwallex was offered $800 million for its shareholders on the capital table, a further $350 million for its founders, and an additional $25 million for key employees. It was a dizzying offer that left Zhang conflicted. “If you think about it, from the end of 2017 we didn’t really have a business [and by] 2018, everything is exploding,” Zhang said. “In 2017, we’re worried about whether the company is going to exist. It would be a good outcome if you get to $100 million…Then you get a billion dollar acquisition offer.” It seemed too good to turn down.

Beyond the bid itself, the esteem with which Zhang held his counterparty added to the allure. Stripe was an undoubtedly impressive organization run by gifted technologists he could imagine working with. “If I was to sell to anybody, Stripe is probably the best buyer and extremely smart. By any means, I feel like Patrick is smarter than me – in all dimensions,” Zhang said of Stripe’s CEO. “You very rarely meet someone with the same vision or ambition but just smarter than you. And younger than you as well.” Why fight for market share against someone with both intelligence and time on their side?

Zhang could also appreciate the merits of the deal. Stripe had built America’s brightest insurgent payment system. It boasted strong infrastructure and a well-constructed application layer. Airwallex looked like the missing piece. Though Zhang’s team had yet to build an application layer, it had constructed robust piping to many of the most critical markets Stripe had yet to win. Together, they’d be unstoppable: a global provider with leading infrastructure across card networks and banks, and a set of useful applications. “Stripe didn’t have any of the products we had,” Zhang said, referring to some of the functionality of Airwallex’s global money movement network. “And we didn’t have what Stripe had,” he added, referencing the Irish-American firm’s payments processing and credit card offerings. “We wanted to build into each other’s space. If Stripe bought us, they would accelerate themselves by many years.”

Discussions continued with Stripe’s management team flying to Melbourne for further due diligence. Kai Wu found himself at the heart of these conversations, just three months into his Airwallex career. Wu had joined Zhang’s startup that summer as Head of Strategy, leaving a cushy role at Boston Consulting Group. He departed the corporate world in search of excitement, animated, as Zhang had been, by approaching his fourth decade. “I was 29 and looking for some adventure,” Wu recalled.

Stripe’s offer was proof Wu had found what he was looking for. Stepping into a temporary CFO-style role, Wu operated opposite Will Gaybrick, collaborating on the finer details. But as much as Stripe’s interest delivered the excitement Wu had craved, it also threatened it. Yes, he would hold an impressive-sounding job at a subsidiary of an impressive organization. But where was the jeopardy in that? “It’s better to be a pirate than join the navy,” Steve Jobs once remarked. Wu had finally escaped the pin-striped embrace of the corporate world, only to find himself facing down another kind of uniform.

The rational decision was to sell. Zhang knew it, Wu knew it, and CTO Jacob Dai knew it. And yet, when they talked it through, it all felt uninspired, almost pointless. “I remember I had a discussion with Jack and [Jacob],” Wu said. “Like, ‘Are we just going to retire?’ Because if we’re bought out by Stripe, then suddenly, we become a subsidiary. And we know that when we become something like this, we won’t really have the ambition we used to have to build and grow the business.”

Wu’s articulation mirrored Zhang’s assessment: it was simply too early to cash out. Especially when so much excitement and opportunity lay ahead. “If we got merged into Stripe, we would just become a division of Stripe, and that’s just less interesting to us. At the end of the day, it wasn’t a monetary decision,” Zhang said. Airwallex turned down Stripe’s offer.

Usually, when such stories are told, when we recount the tale of the bold founder who turned down billions, their triumph is assured. Whatever riches they rejected have been repaid many times over, vindicating their self-belief. Zhang knows that is not yet true in his case. “If you think about Stripe stock in 2021, that went 10x from when we were talking with them,” he said. “I’d be worth multiple billions myself.” Stripe’s valuation has been given a haircut since then, alongside many other tech companies, but the overarching point remains true.

Though Zhang had never been one to waste time, Stripe’s interest revealed the race Airwallex was now in. Finding extreme product-market fit was an achievement that served to beget more challenges. If Airwallex wanted to keep growing and realize the lofty ambitions it had pitched to Gobi and Sequoia and Tencent and Square Peg, it would need to outmaneuver exceptional businesses like the one Patrick and John Collison had built. “I know Patrick pretty well and I know that he’s a smarter guy than me. So I have to work twice as hard to catch up.”

The first move Zhang made was setting in motion a plan to build an application layer. Up to that point, Airwallex had focused exclusively on its infrastructure. “Even until the Stripe acquisition, the vision was very much ‘build the best financial infrastructure in the world to power global payment’” Zhang said. “Basically, [we wanted to be] the payment network connecting any digital payment endpoint to any other digital payment endpoint.” Whether the sender had money in a bank account, on a card, or in a digital wallet, Airwallex was built to ensure it could reach any destination. In doing so, the startup was disrupting traditional banking and card networks, unifying them into a single system.

The conversations with Stripe had revealed the opportunity building out applications offered, as did demand from Airwallex’s existing users. “Some of our customers were saying, ‘Hey, we want to try your product. We also need our operations team to use your product for payments – we need a software layer on top of the infrastructure.’”

Airwallex broke ground on this initiative in 2018, and in 2019, its efforts began to bear fruit. Zhang would devote considerable resources to building a robust application layer in the following years. Look at Airwallex’s product suite today, and you’ll find global business bank accounts, bill pay functionality, borderless cards, expense management, an FX interface, and more. What once looked like a weakness has become a strength.

Frozen

One reason fintech is such a compelling sector to invest in is its proximity to money. It is obvious to the point of idiotic to say that every startup, every business, wants money. Financial products – the applications we use to invest, the systems our businesses rely on to process payments – touch, hold, and move that money in the regular course of their operations. While most startups have to wait to make a sale to access your money, fintechs just have it. That immediacy opens up unique revenue generation opportunities, whether through the float, interest, or something else.

Though an advantage in one respect, fintechs’ intimate acquaintance with funds makes them particularly susceptible to bad actors. It is almost a rite of passage for an early-stage fintech company to endure a spate of fraud that takes advantage of a firm’s immaturity.

Airwallex endured its rendition in 2019, though, in truth, it owed more to misfortune than mismanagement. That year, two of Airwallex’s Hong Kong customers defrauded a Uruguayan company, resulting in the city’s police department freezing $18 million in funding and initiating an investigation. At the same time, Airwallex, led by Chief Legal Officer Jeanette Chan, began investigating its policies.

Chan had joined Airwallex just a few months earlier after a 33-year stint at blue chip law firm Paul, Weiss. She had never expected to leave her post in Hong Kong. “I always thought I was going to retire from Paul, Weiss and have a lovely, peaceful, relaxing life after that,” Chan said. An encounter with Jack Zhang changed those plans. “What drew me to Airwallex was really Jack. I met up with him a few times, and was blown away by his passion and vision of what he really wanted to do.” She joined in 2019 to scale Airwallex’s legal and compliance function, joining a startup with just three licenses in Australia, Hong Kong, and the United Kingdom.

The fraud incident in her home city paused Chan’s efforts to scale her team, requiring her full focus. “It was quite a massive undertaking,” Chan said, requiring constant communication between the company, employees, customers, investors, and regulators. Chan got to the bottom of it, figuring out exactly what had happened. She was encouraged to discover that Airwallex had complied with all the necessary regulations in onboarding the nefarious customers. “I was really thankful that there was nothing [we did wrong] – we did everything by the book…We asked all the questions, we checked all the boxes.”

Unfortunately, the Uruguayan company had fallen victim to a phishing exploit. The scammers had contacted the firm’s CFO and asked them to wire money to a certain address. He had done so, believing them to be a legitimate partner. Although it was a nightmarish event for the victim, it wasn’t something standard KYC and fraud prevention necessarily could have prevented. Nevertheless, Airwallex worked to return the Uruguayan firm’s capital. “I discussed it with the victim, and we came up with an agreement. And they realized that they were the ones that were a little bit careless.” The regulators appeared to reach the same conclusion, permitting Airwallex to keep operating in Hong Kong.

For Chan, the episode served as a vital lesson. “From the company’s perspective, I thought it was a good wake-up call for us,” she said. It was an early stage of our company, we were just four years old. An incident like that really slaps you in the face. It makes you say, ‘Oh my god, we’ve done everything. These fraudsters are there, they’re never going to go away, and they get smarter and smarter and smarter. So we have to be smarter and smarter and smarter than them. And always one step ahead of them to detect what they’re up to.”

Even though Airwallex hadn’t caused the fraud, Chan still felt the firm needed to improve. In its aftermath, she encouraged Zhang to devote resources to strengthen Airwallex’s defenses. “We tightened our onboarding process, we tightened our transaction monitoring process,” she said. “To us, it’s not how much business we do, it’s how much business we do in a safe and compliant manner.”

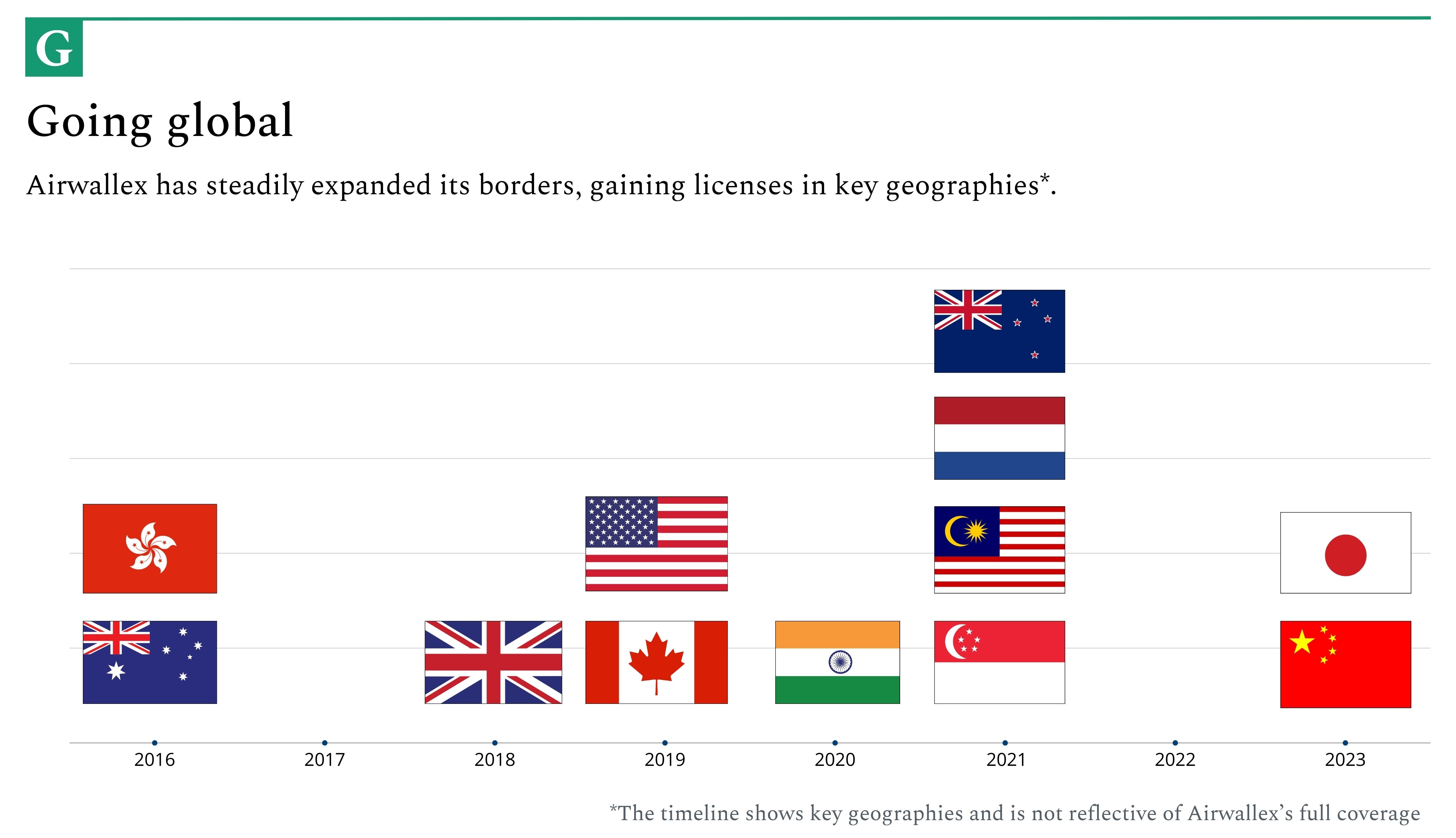

Chan was critical in handling the Hong Kong fraud and has established herself as a key player over the intervening four and a half years. Today, Airwallex has more than 60 licenses and registrations, spanning Asia, Europe, Oceania, and North America. It has also begun to grow its presence in Latin America, with licensing applications in process for both Mexico and Brazil.

Holding the necessary licenses can sound like a bureaucratic formality, but it tangibly impacts Airwallex’s product. When Brex was evaluating payment processors, this embedded global availability stood out to Marco Mahrus. Over four years at Brex, Mahrus served in several roles, most recently as Chief Business Officer. “Airwallex spiked most fundamentally on the basis of how they believe it’s important to be directly licensed in all the main regions to enable the most control over how they do money movement,” Mahrus said.

As Mahrus explained, indirect payment systems often introduce frustrating complexity and added cost. “When you do a SWIFT payment, a customer can send money through their bank [which] would then connect to another payment service provider’s bank partner – and to get to that bank, they go through two correspondent banks. And then that payment service provider is trying to move money to Brex’s bank account – and would have to go through two more correspondence banks,” he said. “Literally, it could take 30 days, or you could lose track of payments. If you do too many hops [or] somebody in the chain drops one of the messages associated with that payment, suddenly you don’t really know who the payment is from and who it’s for.” Without direct access, money flowed through a confusing concatenation of accounts and entities, jumping from one to another. By using Airwallex, Brex cut out these unnecessary convulsions. “When somebody is licensed for money transmission, they end up needing to use [fewer] corresponding and partner banks. There are fewer hops in the system, less expense, [and] less latency.” Today, Airwallex is one of Brex’s “main partners” for international money movement.

Though Chan’s team has been critical in building the regulatory moat that has attracted customers like Brex, the CLO sees new hurdles on the company’s horizon. “As we develop more and provide more new services and products, it becomes all the more important to have a very robust risk and compliance program.” Chan knows her team must balance international ambitions with domestic rules to do that. “I tell the team, ‘Think global, act local.’”

In 2020, Airwallex’s ability to operate at scale around the world was tested.

Winning the world

By the turn of the decade, Airwallex had established itself as the preeminent cross-border payments startup in APAC. It had regional competitors – not to mention the behemoths in the US and Europe eyeing its market share – but the caliber of its product, influential investor base, and strong traction had helped it separate from the chasing pack.

A more conservative CEO might have been content with this position. Airwallex was on its way to owning one of the world’s most consequential and lucrative regions. It had signed up major customers, but in the grand scheme of things, its market penetration was minimal compared to what it might one day attain. A reasonable strategic plan would have been to double down on its focus area, digging deeper regional moats and establishing stronger brand recognition in existing markets.

But Jack Zhang is not reasonable. An investor who spoke to Zhang around this time outlined the Airwallex CEO’s aggressive plans for expansion. He didn’t simply want to own APAC but to conquer the world, becoming the dominant provider across Europe, North America, Latin America, and beyond. At the same time as he grew Airwallex’s frontiers, Zhang planned to radically expand its product offering, layering on new applications. It formed an “out and up” approach to market growth.

The investor was impressed by Zhang’s ambition. “We look for spikes in people. Even if they’re ok in other stuff, if they’re truly exceptional in certain parts, we find that generally those people tend to outperform,” he said. “Jack, I would say, has some of those spikes in spades, right? He is very intense, he moves very quickly. He is very, very ambitious.” The financier in question would go on to invest in one of Airwallex’s growth rounds.

Many other venture firms reached similar conclusions about Jack Zhang and his company during this period. Airwallex first achieved a billion-dollar valuation shortly after turning down Stripe’s acquisition offer in 2018. In the following three years, it would see that figure spike sharply, jumping from $1.8 billion to $2.6 billion to $4 billion to $5.6 billion across four new fundings. New investors like Lone Pine Capital, Greenoaks, and Salesforce Ventures helped deliver $600 million in fresh capital.

Such lavish raises were a product of a fizzing bull market as well as Airwallex’s snowballing traction. From 2020, it expanded its geographic reach to the US, UK, Europe, Singapore, Canada, and Israel. It secured additional licenses or registrations in markets such as Singapore, Malaysia, Netherlands, Lithuania, China, and Japan.

At the same time as Airwallex expanded its scope, it worked to deepen its hold on the Asian markets. In late 2020, Kai Wu also began the lengthy application process that would result in Airwallex securing a Chinese payments license in early 2023 – becoming just the second foreign company to do so after PayPal. You would be forgiven for thinking Airwallex must have already had such a license, given how critical China had been to the company’s growth and how aggressively Zhang had pursued customers like Tencent and JD.com. Though Airwallex was able to operate in China from its earliest days, it relied on a common but suboptimal partnership model. Rather than holding the license themselves, Airwallex relied on local license holders. While this approach was functional, it left Airwallex open to regulatory risk. Notoriously protective, Zhang and Wu knew that the Chinese government could alter its rulebook to outlaw this partnership model at any moment, freezing out foreign players. (It was a farsighted maneuver: in December 2023, China published new rules that potentially curtail this practice.)

To de-risk the situation, Airwallex obtained a license of its own. Though that may sound like a simple procedure, the reality was far from it. For the past “six, seven years,” China has not issued a net-new payments license, according to Wu. As such, the only way to get one is to purchase an existing license-holder, acquiring a local Chinese company. This is the easy part. After a company decides on a target, regulators must approve it. In Airwallex’s case, that proved a painstakingly sluggish process. “In three months, I found a deal and convinced the business owner to sell,” Wu said. “[It took] three years to get approval.”

As Airwallex opened up new markets, it also began to win new customers. In 2020, Airwallex processed approximately $10 billion in volume. The next year, it managed roughly $17 billion. Despite this rapid growth, Airwallex managed to maintain a high level of customer service. Michael Sindicich, CEO of Navan’s expense division, emphasized this aspect of Airwallex’s offering. After joining as a customer in mid-2022, impressed by Airwallex’s global availability, Sindicich was struck by the thoroughness of customer support. “The attention we get all the way down from Jack [is notable],” Sindicich said. “We even have a shared Slack channel between our developers and product team and [Airwallex] and Jack is always commenting there and jumping on stuff. I’ve never seen a founder of such a big company that’s so hands-on and in the weeds.” Sindicich summarized Zhang’s omnipresence neatly: “I don’t think Jack sleeps. Or takes any vacation.”

Remarkably, such attention does not seem to be limited to multi-billion dollar organizations. Emily Chu, CEO of snack company Hey! Chips also referenced the ease with which she can lean on Airwallex’s team. “We’ve been in a group chat the whole time,” Chu said. “So whenever I see a problem, I ask them.”

Though Airwallex appears to have maintained a strong level of service during its hyper-growth in 2020 and 2021, other issues came to the fore. A recent piece called into question staff screening procedures during this period, a critical function for an organization operating in the sensitive financial realm. The article reports on the findings of an internal audit commissioned by Airwallex, which recommended leveling up the company’s screening process. “The audit didn’t uncover any breach of applicable regulations,” CLO Jeanette Chan remarked, “But it was a reminder that we need to constantly reevaluate and uplift our procedures to keep up with the business’s growth.”

Airwallex’s cultural decline was another symptom of an organization struggling to keep pace with its ambition. Zhang pushed overburdened employees to work faster and harder than ever to meet demand. Never the most diplomatic of communicators, Zhang’s decision-making and communication became even sharper, faster, and terser – perhaps to meet Airwallex’s rapidly changing reality. To some, his language could border on rude. To others, it went far beyond it.

The implications of the global pandemic exacerbated such issues. As Pranav Sood, Airwallex’s EGM of EMEA, remarked, “The company’s expansion from a revenue perspective and a people perspective really happened in 2020 and 2021. But something else happened in 2020 and 2021 as well.” That “something else” required Airwallex to embrace a fully remote model at the same time that it hired rapidly, contributing to a disconnected and dissatisfied workforce. Employees were dictated decisions with little explanation, forced to follow a leader many had never met.

Posts on Glassdoor and other sites gave voice to the issue, and as with nearly all anonymous review platforms, comments coalesced around the tails, alternating between scathing and glowing. One post issued in 2021 summarized the state of Airwallex with admirable equanimity: “Growing in a messy way.”

Starting in 2022, with the pandemic retreating in the rearview mirror, Airwallex started reworking its organizational structure. In particular, Zhang took a federated approach, turning the company’s different regional units into semi-sovereign entities with discrete teams and leadership. Kai Wu became EGM of APAC, while Airwallex hired former GoCardless VP Pranav Sood to take over EMEA. While Ravi Adusumilli initially joined from Pinterest to manage partnerships, after 18 months, he also became EGM of the Americas.

For Sood, the autonomy afforded by this model was particularly appealing and differentiated. “[It was] one of the things that really drew me here. It’s quite rare to have an operating model where the individual regions are given the license to operate and build with a degree of freedom and independence,” he said. “Typically speaking, when you look at SaaS org structures and operating models, it’s often the case that the head office dictates how things are going to work. Then you have GMs in different markets who are effectively VPs of Sales, whose job is to execute against your GTM plan that’s basically been dictated for them. Whereas at Airwallex, Jack’s philosophy is that for us to be a successful global business, we need to build local businesses. That means in EMEA, you build an EMEA business, and figure out what needs to happen for customers in the UK, Europe, or the Middle East to want to work with you.”

Adusumilli seconded Sood’s assessment. “It’s not like a top down culture or anything like that. But [at the same time] we keep in mind the overall Airwallex global mentality,” he said. “That’s the balance I’m trying to strike.”

As well as refactoring Airwallex’s regional structure, Zhang added leaders to help address the company’s unhappy employee base. Jon Stona joined as VP of Marketing from rival Stripe with a mandate to calibrate that function and amend its hiring practices. Recruiting Richard Yan as VP of Talent was an even more direct attempt to address the issue. Today, Yan serves in an even more expansive role as VP of People & Talent.

Airwallex ended 2022 with a stronger structure and refreshed leadership. It had endured the challenges of the pandemic and made it to the other side as a larger, more global, more fully-featured, and more valuable business. After the tumultuousness of the past few years – the near-death scrapes and regulatory wrangles – Zhang might have hoped 2023 would bring much-needed stability. Instead, Airwallex’s cultural issues rose to a head.

Rules of engagement

Shannon Scott joined Airwallex in December 2020. Though Scott had briefly overlapped with Jack Zhang at the University of Melbourne’s computer science department, they’d taken very different paths post-graduation. Rather than hopping between jobs in traditional finance and filling his weekends with side projects as Zhang had, just a few years after receiving his degree, Scott took a role at an up-and-coming defense company, Palantir.