Stablecoins: The Next Financial Platform

Stablecoins are more than just an asset – they’re the foundation for a modernized financial system.

Brought to you by Tegus

Are you spending too much time skimming expert transcripts or digging for insights so you can make powerful investment decisions?

Powered by advanced AI and machine learning algorithms, Tegus’ platform supercharges your research process so you can extract valuable insights in seconds. We summarize each expert transcript so you can assess key questions and themes before digging deep. But that’s not all—Tegus now auto-tags topics discussed both within a transcript, and across transcripts for a company so you can quickly assess if you want to dive deeper into content.

Increase your research efficiency and reduce your time to insight with Tegus’ latest innovations in AI.

If you only have a few minutes to spare, here’s what investors, operators, and founders should know about the promise of stablecoins.

- Stablecoins solve real problems. Stablecoins provide the ability to move value freely across borders, at the speed of the internet, with the ease of a text message, in a safe and low-cost way. Whether you’re an individual in Nigeria wanting to hold a stable currency or a multinational corporation managing cross-border payments, this is a big deal.

- Stablecoins have signs of product-market fit. There are ~$125 billion of stablecoins outstanding and ~1 million daily active wallets that use stablecoins. There is no denying that people worldwide use stablecoins daily.

- Stablecoins are more than just an asset; they’re a platform. Stablecoins allow for the creation of an open, cheap, and programmable global payments system. They aren’t a singular asset (in fact, many versions of them already exist) and should be viewed as a financial infrastructure layer that significantly upgrades how value can be held and transferred.

- Stablecoin issuers have a clear business model. Unlike most crypto companies where the path to monetization is murky, stablecoins have a clear profit engine. Stablecoin issuers monetize float on the collateral they hold in reserves and can offer value-added services to their customers over time. They look less like speculative crypto projects and more like next-generation banks and payment processors.

- Stablecoins will penetrate the real world over the coming years. While US regulators send mixed messages about stablecoins, other countries embrace them. More importantly, a mix of start-ups, growth-stage companies, and traditional financial institutions are building products designed to take them mainstream. Even if they don’t realize it, consumers will likely use stablecoins soon.

Note from the editor

The Generalist occasionally invites guest contributors to share their thoughts. We do so when we believe the person in question has strong expertise in the subject matter and a thoughtful perspective.

This piece comes from a pseudonymous contributor, Basho, a long-time researcher and investor. Through conversations and reviewing prior private work, we were impressed by Basho’s prudent but optimistic view on crypto. We especially enjoyed the manner in which he laid out the stablecoin landscape and felt it would be valuable for Generalist readers. We collaborated to adapt Basho’s research for this piece. You can see more work by Basho on their Substack, Deeper Knowing. As a final note, Basho’s identity and professional background is known by The Generalist team.

Few creations have stronger product-market fit than the US dollar. Though controlled by the American government, dollars are desired around the world, prized for their stability. The owner of a corner shop in Lagos or a hostel in Buenos Aires happily accepts payment in greenbacks because they hold their value much better than local currencies. While the purchasing power of the naira or peso fluctuates sharply yearly, the dollar holds. Given the opportunity, many would prefer to earn, spend, and save in USD – or something similarly robust. Domestic regulations and operational constraints typically make that dream either explicitly illegal or simply impossible.

Stablecoins provide a solution. As the name implies, these digital currencies maintain a fixed price relative to a reference asset – typically the US dollar. Unlike much of the crypto landscape, stablecoins offer no dramatic run-ups and speculative gains. They are designed to maintain their value, to act like a dollar in digital form.

Admittedly, it is a strange time to make a crypto* bull-case. The past 18 months have shown the sector in its worst light, revealing spectacular fraud and widespread gambling-esque behavior. Current headlines often make for bleak reading, foretelling irrational regulatory crackdowns and further debacles. There is good reason to be dismayed by the lack of real impact the category has made and to question the technology’s ability to solve genuine problems.

Despite these issues, I believe crypto’s transformative promise remains intact. Though 99% of activity in the space may have been noise, the 1% of companies building meaningful products will, I believe, dramatically impact the world, creating significant enterprise value in the process. Understanding where this conviction comes from requires looking below the surface and examining the primitives being built and what they unlock.

Stablecoins represent one of the most concrete examples of crypto’s promise, protecting individuals against currency devaluation, accelerating and reducing the cost of global payments for businesses, and building infrastructure for a more open, accessible financial system. At a fundamental level, stablecoins aren’t merely a new asset but a radical new platform.

In today’s piece, we’ll explore what stablecoins are, how they work, and why almost a million crypto wallets transact with them daily. We’ll unpack how enterprises like Stripe play in the space and how the technology could impact both businesses and consumers. To conclude, we’ll analyze the main players and explore which models might win in the future.

Stablecoins as a platform

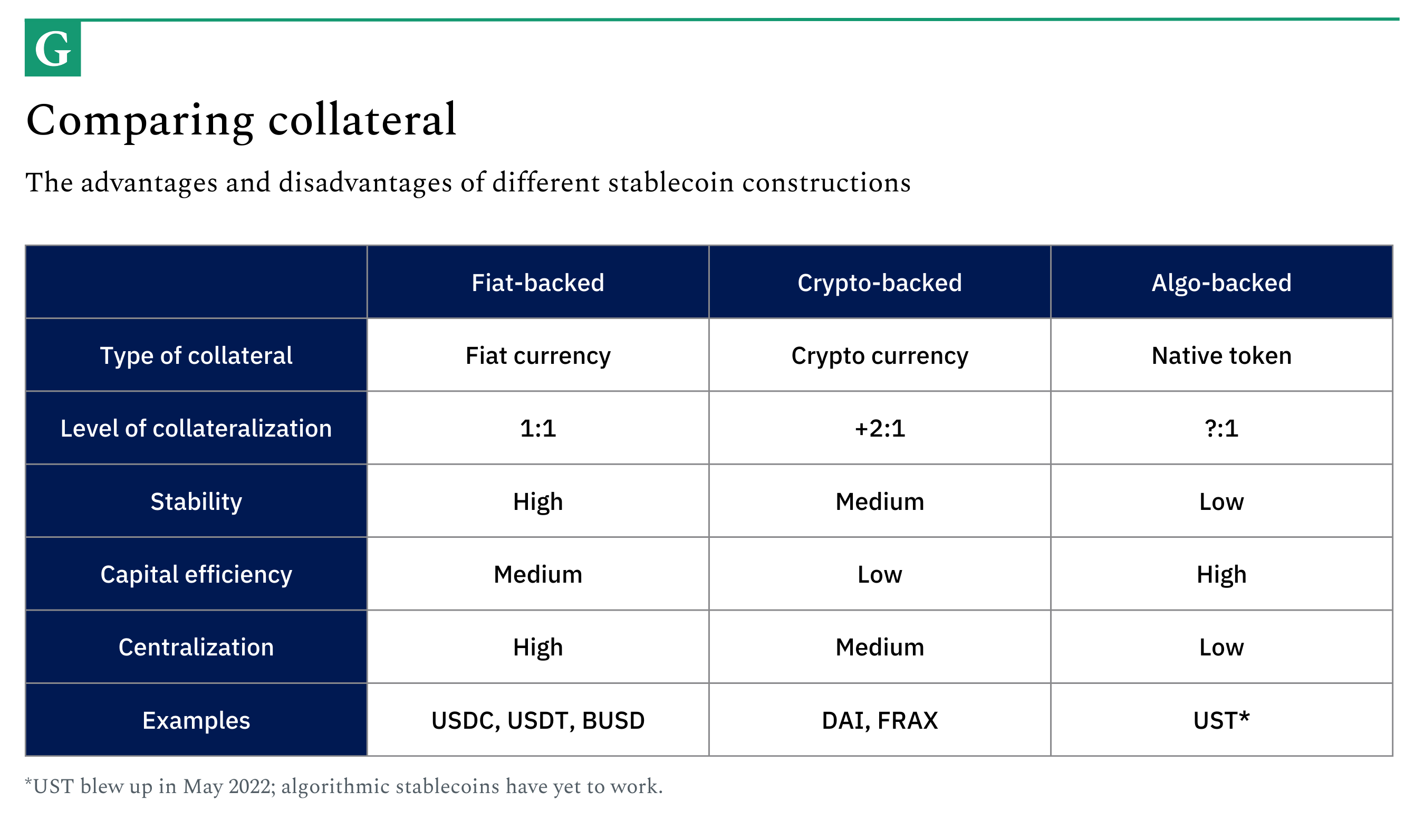

Stablecoins are designed to maintain a fixed price, but not all are created equal. There are three primary types: “fiat-collateralized,” “cryptocurrency-collateralized,” and “algorithmic.” We’ll focus on the first category in today's piece, but it’s worth understanding all three.

Fiat-collateralized stablecoins are the most straightforward. A corresponding, real dollar is held in a bank account for every synthetic dollar printed on a blockchain. A clear 1:1 ratio between the stablecoin and the fiat currency supports its value. The result is a high-stability currency with reasonable capital efficiency since you can scale the circulation of your stablecoin linearly with the dollars you have on hand. This method also comes with a high centralization risk. Your real dollars are held by a financial institution somewhere, which could be frozen. If that were to happen, your stablecoin might take a hit. USDT (Tether), BUSD (Binance and, until recently, Paxos), and USDC (Circle in partnership with Coinbase) are all examples of fiat-collateralized offerings.

Cryptocurrency-collateralized stablecoins make different trade-offs. Rather than securing the currency’s value with fiat, this category relies on crypto. For every synthetic dollar added to the blockchain, cryptocurrencies like ETH are secured in a smart contract worth more than the stablecoin. For example, for every $1 of value added to the blockchain, $2 in crypto might be used to back it. Smart contracts automatically liquidate holdings when ratios fall below certain thresholds to manage collateralization. This type of stablecoin has moderate stability, low capital efficiency (given the over-collateralization), and lower centralization risk. Currencies like DAI (MakerDAO) and FRAX (Frax) fit this group.

Finally, we have algorithmic stablecoins. Synthetic dollars added to the blockchain are backed by nothing – except the native token of the stablecoin itself. Yes, it’s as wild as it sounds, which is why it hasn’t worked to date. UST (Terra) was the leading example until May 2022, when it blew up in spectacular fashion. In theory, algorithmic stablecoins have low stability, high capital efficiency (you effectively print money!), and minimal centralization risk.

While crypto-collateralized and algorithmic stablecoins are interesting and have valuable applications, most current usage is in fiat-collateralized. This category also represents the largest opportunity for the foreseeable future, though some crypto-native readers might take issue with that claim.*

Benefits

Before considering adoption, it’s worth noting how this asset improves upon traditional money and financial systems. In short, stablecoins make money programmable, permissionless, borderless, and interoperable. Meanwhile, stablecoin infrastructure allows money movement to happen faster and cheaper. Let's spell out these transformations to avoid sounding like empty buzzwords.

Firstly, stablecoins make money programmable. When money is natively embodied in code, it can be manipulated like software. This unlocks a wave of new uses and applications. Suddenly, you can tell money to do things – to act or interact with other applications in certain ways. In the future, application developers will use smart contracts to program money into fascinating, valuable configurations.

Next, stablecoins make money permissionless. Owning a stablecoin is like holding cash in digital form. That’s very different than having money in a bank account. You can give it to anyone you want without relying on third parties. It is the equivalent of handing someone a $20 bill, but over the internet. That’s powerful not only for consumers that use stablecoins, but for developers that want to build financial applications freed from the legacy banking systems’ constraints.

Third, when replaced by stablecoins, money becomes borderless. Blockchains create what looks like a globally unified financial system. There are no international borders in stablecoin payments, allowing wallets across the world to interact with each other easily. A user in Mexico can send money to a friend in Egypt seamlessly.

Fourth, stablecoins introduce interoperability to the financial system. Suddenly, your “dollar” can interact with any application. You can send money freely from Venmo to Cash App and back again without going through intermediary steps. Walled gardens no longer exist. Not only is this a radical improvement for consumers, it’s an unlock for developers and opens up a rich design space for financial application development.

Finally, stablecoin infrastructure makes money movement faster and cheaper. The removal of intermediaries results in the near-instantaneous transfer of funds and settlement. The idea of a wire transfer or international payment being pending doesn’t exist with stablecoins. Moreover, such capabilities are available 24-7-365. That beats the hours of operation for every bank on Earth. The removal of banks – and their associated cost structures – should dramatically drop the cost of money transfers. At full scale, blockchains should facilitate value transfers that cost just fractions of a penny. Such economic benefits are good for customers, of course. They also open up new business models like micropayments.

These are all compelling benefits, but what would a mature stablecoin ecosystem feel like in practice? My hope is that it would resemble an open, cheap, and programmable version of Venmo that spans the globe. It would provide the ability to send money to anyone, anywhere, regardless of what application they were using. It would offer low fees and enhanced functionality, powered by the wide range of dynamic applications built on top. If executed correctly, it would be financial infrastructure that appealed to everyone: retail consumers (think WeChat Pay for the entire world), enterprises (imagine B2B payments on stablecoins), and financial institutions (streamlined operations across the board).

And while it’s fair to say that stablecoin infrastructure has yet to fulfill all these promises, they are within reach if development continues at its current pace.

Adoption and usage

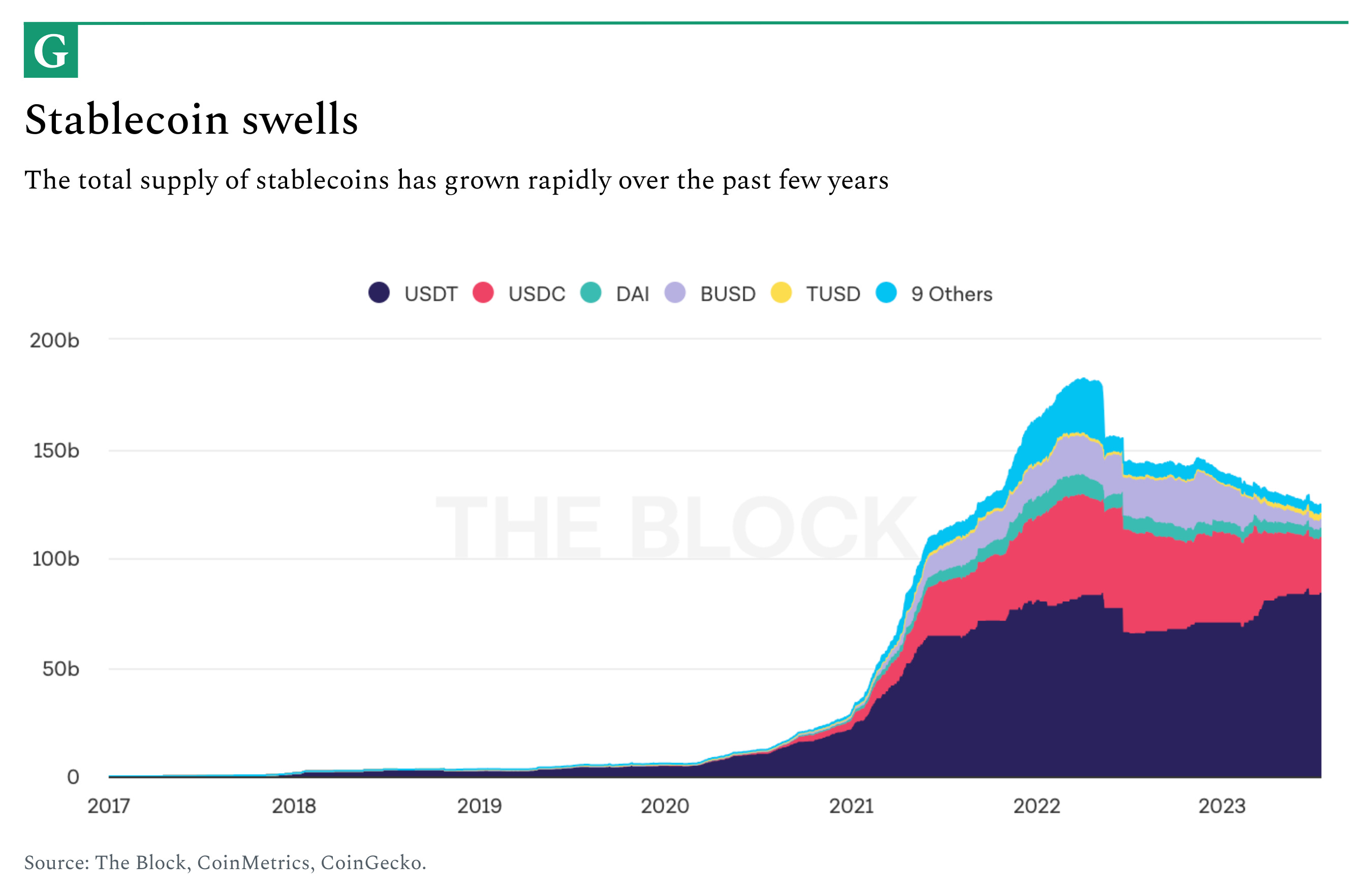

Though still in its early stages, stablecoins see widespread usage. There are roughly $125 billion of stablecoins in circulation, of which over 90% are fiat-collateralized. Approximately $80 billion of the total exists on Ethereum, while most of the remaining $45 billion exists on Tron, a blockchain popular outside of the US that sees heavy usage of USDT. As demonstrated by the graph below, stablecoins have grown rapidly over the past few years:

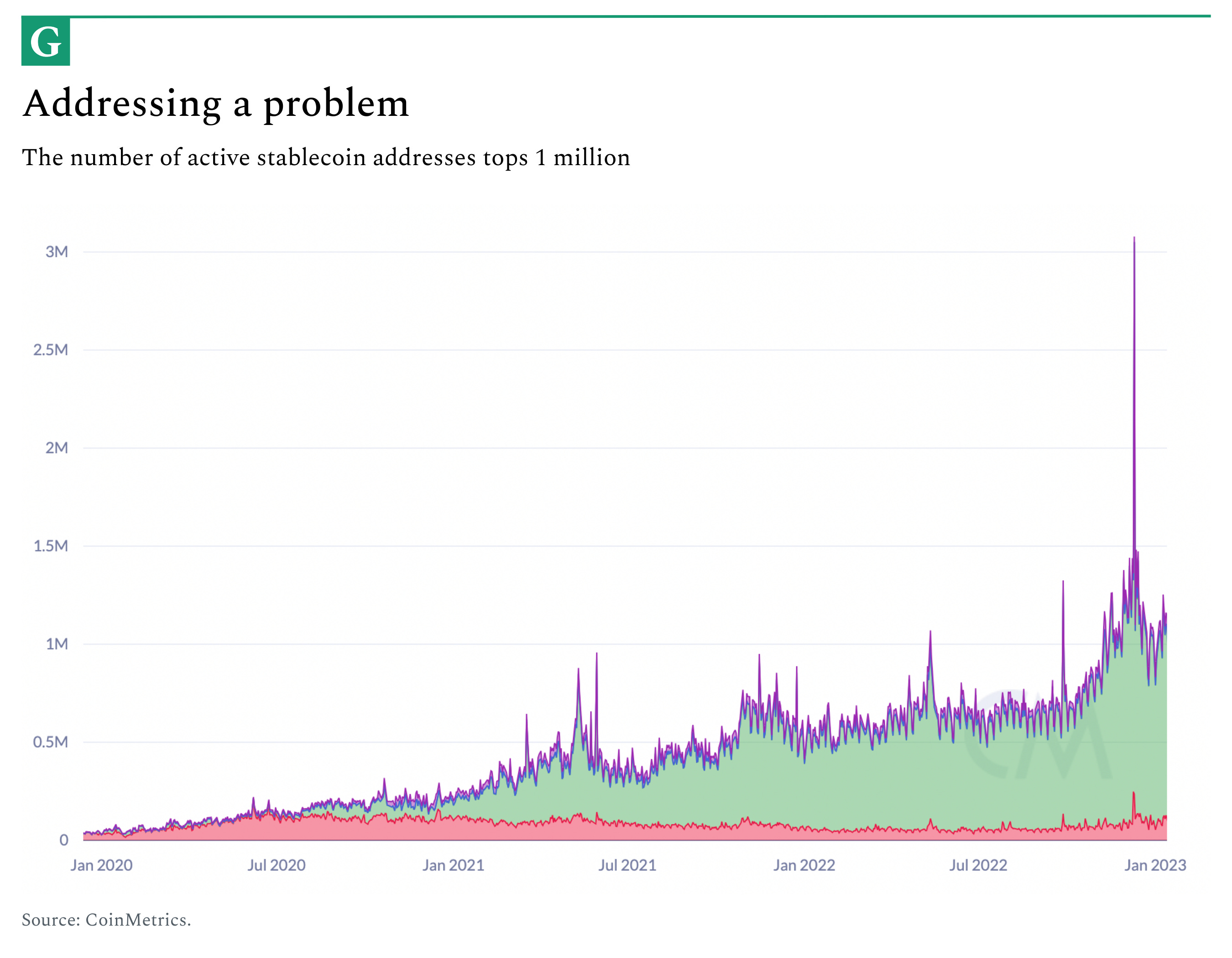

In 2022, users transferred $7 trillion in stablecoins (an average of $20 billion daily), and today there are approximately 1 million daily active wallets using stablecoins. All told, more than 30 million wallets hold a stablecoin of some kind.

As the graphs above illustrate, stablecoin usage has shown remarkable resilience in the face of the Terra collapse and a broader crypto winter. What’s driving this utilization?

Today, the primary use case is from crypto natives – specifically traders – who rely on them as a stable asset for investing and settlement purposes. While this endemic usage has been a major driver of stablecoin growth over the past few years, it’s nothing to get particularly excited about. It creates a floor for stablecoin demand but is unlikely to catalyze broad societal adoption.

What about stablecoin usage in the “real” economy? While it’s the early days of stablecoins’ penetration outside of crypto, there is real world traction. This is apparent by looking at the data – stablecoin wallet balances and sending patterns suggest usage by real people, not just crypto traders. It’s further validated by the anecdotes you hear from users around the world: the interior designer in Nigeria, the developer in Mexico, and the business owner in Argentina.

What will catalyze stablecoins achieving more widespread adoption? Usage is likely to occur where stablecoin functionality offers a meaningfully better experience than the status quo. In many instances, customers won’t know they are touching crypto, as the stablecoin infrastructure will exist behind the scenes (in the same way the average user doesn’t realize they are using the ACH network). Some areas where I’d expect to see adoption are wherever transfer of value is:

- Cross border, where existing infra is inefficient and high cost, including B2B payments (SWIFT is often slow, expensive and non-transparent), P2P payments (remittances cost on average 6.3% of the transaction sent) and international capital markets (like the Eurodollar)

- High administrative burden, where accounting for transaction flows is important (and often expensive), e.g. interbank transfers, securities settlement, loan servicing, and mortgage payments

- Conditional, where you rely on something to occur before payment is sent, e.g. gambling or multi-party transactions

- Related to digital goods, where the item being consumed exists fully in the digital domain, e.g. gaming (or NFTs, if they ever gain widespread adoption)

- In emerging markets, where existing financial infrastructure is not well established, and where access to USD is otherwise limited (e.g. imagine what it takes to open a USD denominated bank account living in Hanoi, and then compare that to spinning up a wallet and buying a stablecoin: it’s a night and day difference)

- P2P, where lower barriers to building financial applications (given less reliance on traditional banks) and the ability to create novel product experiences opens up the opportunity for new consumer applications

- B2B, where having information natively attached to value transfer can be incredibly impactful for operational efficiency, and instant settlement can dramatically alter a company’s working capital dynamics and contracting risk

To make this even more tangible, below are a few examples of how traditional companies are building at the intersection of stablecoins and the real world. It’s worth highlighting that a number of banks and traditional financial institutions are very focused on deploying the technology (albeit, some on “permissioned” blockchains rather than open ones like ETH).

- A Fortune 500 company. This firm currently has USD-denominated bank accounts in 35 countries. The team is exploring moving to a single, centralized stablecoin account to streamline operations. This could result in major improvements in capital efficiency, transparency, and internal business liquidity.

- Visa. The company is piloting a program to settle global transactions in USDC. While Visa can authorize transactions 24/7, it still relies on banking hours to move money worldwide.

- Stripe. The fintech has assembled an entire team dedicated to stablecoin infrastructure. They’ve already launched USDC payments for Stripe Connect customers, meaning you can pay a contractor in Argentina with stablecoins.

- The USDF Consortium. A group of 11 FDIC-insured banks are attempting to tokenize deposits to create more efficient interbank transfers. The consortium is primarily owned by its members and subsequently regulated federally.

- Paypal. Paypal was readying the launch of their own stablecoin, which would have been a major milestone for the space, but pulled the plug on the project at the last minute due to regulatory concerns.

- JPMorgan. In 2020, the bank launched an internal settlement coin dubbed JPM Coin. It powers securities settlement across the firm’s client base. JPMorgan’s longer-term goal is to experiment with stablecoins’ programmability. “We increasingly want you to…actually tell the money what to do,” the team lead noted in mid-2021.

Stablecoins may be in their early innings, but consumers and enterprises are substantively using them. As we’ll discuss later, their utility could expand greatly in the years to come.

Regulatory complexities

Stablecoins are not just technologically disruptive. They pose important geopolitical questions. Indeed, for the US government, they represent both a challenge and an opportunity. On one side, they pose all manner of complications to anti-money laundering initiatives. There are few better financial tools for bad actors than a reliable currency outside formal governmental control.

On the other hand, stablecoins may help promote national strategic interests. What better way to reinforce the USD’s position as the global reserve currency of choice than to get more dollars into people’s hands? Given China’s concerted efforts to shift international capital flows to RMB, the evangelical impact of stablecoins could prove important.

Except for the SEC (*grimace*), US regulators are aware of this potential. Notably, both the House and the Senate have proposed bills to support the existence of stablecoins. For example, Senator Toomey’s proposed Stablecoin TRUST Act outlines a regulatory framework for using “payments stablecoins.” The now-retired Pennsylvania representative laid out the initiative's purpose: “By digitizing the US dollar and making it available on a global, instant, and nearly cost-free basis, stablecoins could be widely used across the physical economy in a variety of ways.”

It’s an exciting vision, albeit not one without risks. Regulators may kill the whole ecosystem. The SEC appears to be attempting this in the US while the rest of the world marches ahead. The European Union, for example, released constructive guidance on crypto markets via something called MiCA. More top down payments modernization initiatives will have an impact on how the market evolves as well. Real-time payments (RTP) networks – for instance Pix in Brazil and UPI in India – may operate in silos, but are already driving innovation in their local markets. Looking further ahead, Central Bank Digital Currencies (CBDCs), which 114 countries representing 95% of global GDP are currently exploring, could make independent stablecoins obsolete.

Time will tell how the government treats stablecoins. I hope that the various regulatory bodies can recognize the technology for what it is: a true platform that can improve the lives of consumers and businesses.

Stablecoins as a business

We’ve established what stablecoins are and how they are being used. But is there a business here? In short: yes. Indeed, issuers benefit from one of the clearest business models in crypto: they can monetize float on their collateral reserve and attach value-additive services. These providers are, in essence, building the next generation of payment processors or banks.

Let’s review how this works and examine how major players attack the opportunity.

Making money

To understand how fiat-collateralized stablecoins make money, we must first go a bit deeper into how they actually work. We know that an actual dollar in a bank account backs each digital dollar. But then what happens?

After the primary issuance (aka “minting”) of the stablecoin occurs, the stablecoin user can do anything with the asset. They could send it to a friend, pay an invoice, trade it for another asset, or invest it to generate yield. In theory, at least, recipients of fiat-backed stablecoins don’t need to worry about the value of the money they’re receiving since it’s backed 1:1. To demonstrate that’s the case, issuers rely on traditional certification methods – attestations from the company itself or third-party auditors. These are released regularly to assure stablecoin users that their money is appropriately collateralized.

As an aside, it’s worth noting that decentralized finance (DeFi)* offers a better attestation method called “proof-of-reserves.” This is because, if the collateral lived in a smart contract, it would be programmatically verifiable by everybody. Since fiat-collateralized stablecoins rely on centralized entities – and there’s no live-feed video of a bank account – that’s not possible here. (FTX is the clearest example of why “proof of reserves” or other robust forms of attestation are necessary. As readers will know, the exchange misused consumer funds that should have been segregated and fully reserved. The company’s fraud couldn’t have happened had it been built on crypto-rails.)

As the stablecoin holder uses the asset as they wish, what does the issuer do with the capital it’s holding? In short, it acts like a bank looking to earn net interest income. It does so by taking the capital in the reserve account and investing it into assets that earn a return. Like a bank, risk management and asset/liability matching are critical to ensuring the account is liquid and solvent. The issuer wants to increase the yield on the reserve as much as possible without taking on so much risk that it undermines trust in the stablecoin’s 1:1 peg with the dollar. As we’ll see below, different issuers take different approaches to asset allocation. The safe approach is to keep cash in well-capitalized banks (a lesson Circle learned after almost losing billions of dollars of collateral in the SVB collapse) and investment assets in highly liquid, highly safe securities (typically, that’s short-duration US treasuries).

To frame the economics, the three primary stablecoin issuers are currently sitting on ~$115 billion, up >20x from early 2020. These deposits earn more than 5% a year (3-month treasuries are yielding 5.4%) and are effectively zero marginal cost. That suggests they’re making more than $5 billion of high gross margin float revenue today. Illustrating the point, Tether announced that it made an eye-popping $1.5 billion profit in the first quarter of 2023 alone.

Given the operating leverage and scalability of the deposit base, it's an attractive economic model. Crucially, the core product can be monetized well without charging fees. That supports higher usage and adoption, which drives more deposits, leading to more revenue.

In addition to float revenue, issuers have adjacent monetization opportunities they’re well positioned to pursue. For example, they can offer crypto on-off ramps, compliance management tools, and treasury services. Like traditional banks, issuers have the opportunity to build a suite of lucrative products, deepening their relationship with customers.

The stablecoin model comes with obvious risks, of course. Can issuers manage the collateral base effectively and minimize the risk of depegging? How will they maintain monetization in a reduced interest rate environment? Will they be able to keep deposit costs at zero, or will competition make it necessary to pay a portion of the float to users? All of these questions will need to be answered along a sustained timeline. Despite the risk, stablecoin issuers have a clear business model and outstanding upside. They look set to become the banks and payment processors of the next generation.

Different approaches

Now that we’ve outlined the business model, let’s take a quick look at the category's major players: Tether (USDT), Paxos (BUSD), and Circle (USDC).

Tether is the unregulated first mover of fiat-backed stablecoins. Owned by holding company iFinex, Tether launched in 2014. With broad global usage, it has become the most widely used stablecoin in the intervening years.

Tether’s success is thanks to its deep liquidity, broad protocol coverage, and, arguably, weaker regulatory supervision. The firm is based in Hong Kong and is not technically regulated in the US. It runs its banking through a Bahamas-based entity called Deltec and has a murky relationship with crypto exchange Bitfinex, owned by the same holding company. As you might expect, Tether is the least transparent of major issuers, including regarding the management of its reserves (which includes assets other than US Treasuries). Indeed, in 2021 the New York Attorney General found iFinex and Tether guilty of deceiving clients and overstating reserves.

Although Paxos offers its own stablecoins (USDP and PAXG), it’s best known as a white-label infrastructure provider. Until February of this year, Paxos acted as the issuer for BUSD, Binance’s stablecoin. Support for BUSD ended after the SEC claimed BUSD was an unregistered security. (Somewhat confusingly, only BUSD was subjected to the SEC’s wrath, not Paxos’ other stablecoin offerings.) The company is regulated by the New York State Department of Financial Services (NYSDFS); Paxos is currently pursuing a de novo national Trust Bank charter. It has a transparent reserve policy and keeps all assets in cash and short-dated US treasuries.

Beyond stablecoin support, Paxos provides various blockchain-focused infrastructure products for third parties. That includes providing brokerage solutions (e.g., adding crypto investment or payments to an application) to PayPal and Mercado Libre; and settlement solutions for securities and commodities trading for clients like Credit Suisse and Koch.

Circle is the full-stack, enterprise-grade player of the stablecoin space. Alongside Coinbase, the company founded the Centre consortium behind USDC. While Circle does the actual issuance of the currency, a revenue-share agreement means that Coinbase also benefits from the float generated*. The company is regulated as a Money Transmitter in most states, is registered as a money service business (MSB) under FinCen, and intends to become a fully chartered commercial bank. It has a transparent reserve policy and keeps all assets in cash and short-dated US treasuries.

Circle’s ultimate goal is to support the use of USDC by building a fully featured financial platform. Its three core product focus areas are payments infrastructure (e.g., API to accept all payment types and settle in USDC), business banking (e.g., treasury management), and crypto services (e.g., custody solutions). It has partnered with companies including Blackrock, Jack Dorsey’s TBD, Visa, and Robinhood.

Ultimately, all three main players take different approaches in the fiat-backed stablecoin space. It’s certainly not clear who will win the market. Will it be an open, independent asset like USDC or USDT? What about a branded offering by someone with distribution a la BUSD or PayPal? Could banks pursue direct issuance if regulatory headwinds lighten up? We are in the early stages of a new design space. The ultimate, winning stablecoin construction could differ greatly from any on offer today.

The broader landscape

It’s worth noting that while our exploration thus far has focused on the existing stablecoin issuers, there is a Cambrian explosion of companies building interesting products in the category. Some are creating valuable infrastructure for the widespread adoption of stablecoins, while others are focused on novel products that use stablecoins as the underlying foundation to offer compelling experiences. All of them are bringing stablecoins closer to widespread adoption, and they provide further insight into what a stablecoin powered future could look like. Although the stablecoin issuers are the dominant players today (and do enjoy a privileged position in the ecosystem), I expect that ten years from now we’ll look back and see that many of the most successful companies in the category, both in terms of enterprise value creation and impact on user behavior, are just getting started today.

Who are these other companies, and what are they building? It would be impossible to cover them all in one post, but here is a quick snapshot to bring to life the wide range of players that are emerging.

Neobanks are building products that leverage stablecoins to provide retail customers a better banking experience. One example is Eco, which automatically converts users’ fiat deposits into USDC in order to unlock a novel rewards offering. Another is DolarApp which offers Latin American users a dollar-denominated account using stablecoins. It protects savings from devaluation and offers cheap cross-border payments. (Editor’s note: Generalist Capital is an investor in the company.)

Next-gen payments companies are using stablecoins to offer new ways for individuals to spend and send money. Companies like Sling (an easy interface for sending money to friends), Bleap (a stablecoin backed debit card that can be connected to any digital asset wallet) and Stables (a stablecoin wallet that is tied to a Mastercard prepaid card) are pushing this frontier.

On the enterprise front, B2B payments focused players like Cedar are using stablecoins to eliminate the frictions of cross-border trade.

And behind the scenes, infrastructure providers are laying the foundations for greater connectivity between both the traditional financial system and stablecoin applications. For example, Monerium has created the ability to tie a digital asset wallet to a specific individual fiat bank account (using the IBAN system), and Bridge is building stablecoin orchestration APIs that provide developers with a way to easily integrate stablecoins into their applications and swap between fiat and different stablecoins.

Looking ahead

We just covered a small snapshot of the experimentation that is occuring in the stablecoin ecosystem right now. Looking further ahead, it’s easy to imagine how improving crypto’s infrastructure could unlock even more exciting stablecoin use cases. Here are a few examples of implementations that could become impactful:

- Embedded payments. When a crypto wallet acts as your single-sign-on (SSO) for the internet, payments are automatically embedded in your browser. In the future, we could effortlessly make micropayments for media, services, or goods we appreciate.

- Tokenized securities. By tokenizing securities, financial market transactions become meaningfully more efficient. In the current paradigm, the administrative burden required to establish ownership, facilitate transfer and actively service assets is massive. (For reference, an estimated $133 billion is spent on post-trade securities clearing and settlement.) In a world with tokenized securities and stablecoins, this friction largely goes away. For instance, a company could programmatically pay a dividend directly to the wallet of a shareholder, and then the shareholder could automatically have those funds reinvested into whatever asset they please – all with zero intermediary paperwork.

- Streamlined verification. Transaction flows can become much slicker when KYC and identity verifiers exist on a blockchain. You’d never have to re-submit fund subscription documents or go through paperwork related to capital calls. Instead, when you invest in a new fund, you could grant the GP permission to check your credentials via an NFT that verifies your Accredited Investor status, and then with a click of a button approve future capital calls from a wallet you specify.

- Dynamic lending. When a company can cryptographically certify details about the state of their business – for example, providing a snapshot of their balance sheet via zero-knowledge proofs or tokenizing the Real World Assets (RWAs) they have as collateral – lenders can issue loans in much more dynamic, real-time ways. For instance, if a lender on a factoring facility can directly see the inflows and outflows tied to a company’s tokenized inventory/accounts receivable, they can disburse capital more quickly and with meaningfully greater confidence.

- Automated rewards. Loyalty programs (and thus pricing and rewards) can become integrated with spending when a consumer’s loyalty status is represented by an NFT. Imagine going to a store to purchase an item, the point-of-sale device pinging your wallet to determine if you have an NFT badge signifying that you’re a top-tier customer, and a 20% discount being auto added into the purchase flow once the NFT’s existence is confirmed. There is no need to ever type in a rewards number, as your loyalty status is embedded into your payment method.

Despite the significant risks, stablecoins represent a technology with extraordinary promise. I would bet that they play a meaningful role in the financial infrastructure of the future. Whether you’re a skeptic or a convert, I hope this piece reveals the category’s real traction (despite market turmoil) and potential to positively impact the broader economy. Crypto has endured a terrible winter, but it still has the power to create meaningful financial innovation around the world.

_____

*Footnote 1 - It is worth stating that crypto needs a serious rebrand. To avoid doubt, when I use the term, I don’t explicitly mean cryptocurrency but the set of technologies (blockchains, etc.) that allow for open and trustless computation. “Open” means that any user can access it, and any developer can build on top without permission. “Trustless” means that platforms built on crypto infrastructure are credibly neutral and verifiably accurate – and that no single party can unilaterally alter the foundations of what is created.

*Footnote 2 - For this group, centralization is one of the great weaknesses of the financial system, as the Silicon Valley Bank collapse underscored. Given their reliance on centralized financial systems, fiat-backed stablecoins cannot offer true peer-to-peer money. I hear that, and I think there are many interesting experiments being run with more decentralized assets that maintain stability, but I believe a massive opportunity exists just upgrading financial rails around the world (as opposed to completely displacing them).

*Footnote 3: The term DeFi is widely used in crypto, but I prefer Open Finance (OpenFi). The exciting thing about the financial infrastructure being built in the DeFi ecosystem is not that it’s decentralized: it’s that it’s open, transparent, and programmable (and, if we are being honest, it isn’t always decentralized). More on this another time.

*Footnote 4: It’s worth noting that the revenue split between Circle and Coinbase is a topic of fierce debate between the two organizations. This is perhaps not surprising given the quantum of money that is at stake. To contextualize, in Q4 of 2022, ~30% of Coinbase’s revenue was from interest income, the lion’s share of which was generated by USDC.

The Generalist’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice. You should always do your own research and consult advisors on these subjects. Our work may feature entities in which Generalist Capital, LLC or the author has invested.

Join over 55,000 curious minds.

Join 100,000+ readers and get powerful business analysis delivered straight to your inbox.

No spam. No noise. Unsubscribe any time.